- Webpages

- Documents

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

For NRI Customers

(To Buy a Policy)

-

![Contact Image]()

Call (All Days, Local charges apply)

-

![Contact Image]()

Email ID

-

![Contact Image]()

Whatsapp

(If you're our existing customer)

-

![Contact Image]()

Call (Mon-Sat, 10am-9pm IST, Local Charges Apply)

-

![Contact Image]()

Email ID

For Online Policy Purchase

(New and Ongoing Applications)

-

![Contact Image]()

Call (All Days & Toll free)

-

![Contact Image]()

Schedule a call

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Give missed call to buy a policy

-

![Contact Image]()

Email

Branch Locator

-

![Contact Image]()

Locate a branch

For Existing Customers

(Issued Policy)

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Call (Mon to Sat, from 10 am to 7 pm, Call charges apply)

-

![Contact Image]()

Email

Fund Performance Check

-

![Contact Image]()

Call (Missed Call)

- Health Insurance

- What it is?

- Coverage

- Features

- Types

- Benefits

- Tax Benefits

- Optional Add-Ons

- Need

- How to Choose?

- How to Purchase?

- How to Buy?

- Who Should Buy?

- Factors Affecting

- Cost and Coverage

- Cover

- Not Cover

- Cover COVID-19?

- Eligibility Criteria

- Fully insured

- Buying at Early Age?

- Procedure

- Documents Required

- Choose the Best

- Compare Online

- Calculate Premium?

- Mediclaim Policy

- Mediclaim & Health

- Key Difference

- Ensure Protection

- Obtain Physical Copy

- Copy of policy online?

- Steps to Renew

- Myths

- To Sum Up

- FAQs

- Related Articles

- Other Cites

- Popular Searches

- Disclaimer

Health Insurance

Health insurance plans can help you manage both planned medical treatments (such as surgeries) and emergency medical expenses (like accidents or sudden illnesses). ...Read More

Explore the range Health Plans by HDFC Life to cover your medical expenses

With Health plans from HDFC Life you can opt for medical insurance at affordable rates

Francis Rodrigues

Francis Rodrigues

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

Vishal Subharwal

Vishal Subharwal

Vishal Subharwal heads the Strategy, Marketing, E-Commerce, Digital Business & Sustainability initiatives at HDFC Life. He is responsible for crafting and ensuring successful implementation of the overall organisation strategy.

What is Health Insurance?

Health insurance is a contract between an individual and an insurance company. The company provides financial coverage for medical expenses as per the policy terms. When you purchase a health insurance policy, you agree to pay a premium every year in return for your medical expenses coverage with prescribed limits.

With most health insurance plans, you can cover health treatments such as hospitalisations, doctor consultations, diagnostic tests, medications, surgeries, etc.

Coverage Types

Health insurance companies offer mainly two ways to pay your medical expenses:

Cashless Treatment: If you are admitted to a hospital within the insurance company's network, you do not need to pay any upfront cost, as your insurer will pay the hospital directly.

Reimbursement Claim: For treatment at out-of-network hospitals, you need to pay for the treatment out of your own pocket initially. You can get a reimbursement later by submitting your hospital bills.

Additional Benefits

Most health insurance plans in India cover ambulance charges, and pre & post-hospitalisation expenses. Additionally, you can claim deductions on your health insurance premiums under Section 80D of the Income Tax Act6. Many policies cover alternative treatments, daycare procedures, critical illnesses and others. However, you should check all the provisions mentioned in your policy documents to utilise the maximum advantage from it.

What is the Right Health Insurance Coverage?

A thumb rule for health insurance is that the coverage should be at least 50% of your annual income. However, due to increasing healthcare costs, experts now recommend a minimum coverage of Rs. 10 lakh. The ideal coverage amount depends on several factors, such as:

- City of Residence: Tier-1, Tier-2, or Tier-3

- Age and Life Stage

- Future Hospitalisation Costs: Depending on medical inflation

For example, a health insurance policy of Rs. 5 lakh coverage amount can be sufficient for young individuals in a Tier-3 city without pre-existing conditions. On the other hand, an older person or someone in a Tier-1 city may need between Rs. 10 lakh and Rs. 20 lakh for better coverage.

Check this table below to get an estimated idea:

Types of Plans |

Metro City |

Urban City |

Rural Area |

Individual Health Insurance Plan |

Rs. 10 lakh+ |

Rs. 7-10 lakh |

Rs. 5-7 lakh |

Family Floater Health Insurance Plan |

Rs. 30 lakh+ |

Rs. 20-30 lakh |

Rs. 15-20 lakh |

Senior Citizen Health Insurance Plan |

Rs. 25 lakh+ |

Rs. 15-25 lakh |

Rs. 10-15 lakh |

Nowadays, the Rs. 1 crore health insurance policies are increasingly affordable and provide extensive protection for critical illnesses or international treatments. By paying an additional premium of just Rs. 1,500, you can get such high coverage.

Otherwise, you can start with a base policy with a lower sum insured and increase the coverage with top-up health insurance.

What are the features of health insurance?

Features |

Health Insurance |

Scope of coverage |

The policy takes care of both preventive and medical treatment that includes screening tests, annual medical checkups, vaccinations, as well as hospitalisation expenses. |

Claims |

Every insurance provider has a cap on the number of claims filed every year. |

Premium |

Health insurance covers an extensive range of services, probably why it requires payment of a higher premium. |

Sum insured |

This is dependent on the plan chosen by an individual. |

Add-on covers |

An individual can choose these based on their requirement. |

What Are the Types of Health Insurance Plans?

There are many different types of health insurance plans available in the market. You can get the following health insurance plans cater to different healthcare needs:

Individual Health Insurance

Individual health insurance policies cover one person's medical expenses for hospitalisation, pre- and post-hospitalisation costs, and daycare treatments. It offers personalised protection for individual healthcare needs and ensures coverage for unexpected medical situations.

...Read More

Family Health Insurance

Family health insurance plans cover the entire family under one policy. This is a simple process and can be more cost-effective compared to individual plans for each family member. Because it includes medical expenses for you, your spouse, children, and dependent parents are all covered.

...Read More

Senior Citizen Health Insurance

Health insurance for senior citizens are specifically designed for older individuals. It provides coverage for medical costs and age-related illnesses and ensures that older adults have access to necessary healthcare services.

...Read More

Critical Illness Insurance

Critical illness insurance cover serious conditions such as cancer, major organ failure, heart disease, and stroke. Upon diagnosis, the policyholder receives a lump sum payment that can be utilised for treatment and recovery without any limits.

...Read More

Group Health Insurance

Group health insurance is a policy purchased by employers to cover the healthcare expenses of their employees. This type of insurance generally needs lower premiums. It often includes immediate coverage without waiting periods for pre-existing conditions, which is beneficial for new employees.

The coverage can also extend to the families of the insured employees to provide total protection for the family members. The employees covered under the same group insurance get the same benefits for their medical expenses.

...Read More

What Are the Benefits of Health Insurance Plans?

Unlock the numerous benefits of health insurance, including:

Financial Protection

Health insurance plans help with medical costs during emergencies. They cover hospital stays, doctor fees, medicines, tests, and other expenses, so you don’t have to worry about paying for your treatment.

...Read More

Cashless Hospitalisation

With cashless hospitalization, you can get medical treatment without paying upfront. The insurance company handles the bills directly with the hospital, making it easier for you.

...Read More

Pre and Post-Hospitalisation Coverage

Health insurance plans also cover costs before and after hospital expenses, like doctor visits, tests, medicines, and follow-up care.

...Read More

Tax Benefits

You can get tax deductions on the premiums you pay for health insurance under Section 80D of the Income Tax Act6.

...Read More

Additional Coverage

Some health insurance plans cover extra costs for pregnancy, critical illnesses, accidents, and other specific health needs.

...Read More

ICU Charges

The ICU charge is one of the major costs in private hospitals in India, where the average range is Rs. 15,000 to Rs. 30,000 per day. With a health insurance plan, you can cover the cost of essential ICU services such as doctor visits, bed charges, nursing care, medical equipment costs, and other essential costs for treatment and monitoring.

...Read More

Maternity Benefits

With health insurance's maternity benefits, you can get coverage for pre-natal and post-natal expenses such as diagnostic tests, doctor consultations, and hospital stays during childbirth. However, to get these benefits, there is a waiting period under every policy, which may vary between 3 months and 4 years.

...Read More

Pre-existing Diseases

If you have any pre-existing disease, you have to complete the waiting period first before you file claims related to your pre-existing condition. Depending on your health insurance company, you need to wait between 1 and 4 years.

...Read More

Tax Benefits with Health Insurance

One of the main benefits of health insurance is financial protection, but there’s more. Health insurance can also help with tax planning. The premiums you pay for health insurance can be deducted from your taxable income under Section 80D of the Income Tax Act6. The maximum deduction is Rs 25,000, which increases to Rs 50,000 for senior citizens.

In that case, the policyholder can enjoy a deduction of up to Rs 75,000 from the taxable income.

If the policyholder and their parents are both over 60 years old, the total deduction can go up to Rs 1 lakh. To claim this deduction, you need to provide receipts for the premium payments and a copy of the insurance policy that shows the names, relationships, and ages of the family members covered.

You can claim this deduction even if you pay the premium through methods other than cash.

Check the below table to learn how much can you claim as tax exemption with different types of health insurance:

Premiums Paid for |

Maximum Tax Exemption |

Individual and family (all age<60 years) |

Rs. 25,000 |

Individual and family + parents (all age<60 years) |

Rs. 50,000 |

Individual and family (below 60 years) + parents above 60 years |

Rs. 75,000 |

Individual and family + parents (all above 60 years) |

Rs. 1,00,000 |

Optional Add-Ons in Health Insurance

With optional add-ons to your health insurance, you can get enhanced coverage and benefits with your health insurance plan. At HDFC Life, we provide several optional add-ons, such as:

Hospital Cash Benefit

This rider benefit provides a fixed allowance for each day of hospitalisation. It helps to cover miscellaneous expenses incurred during your stay.

...Read More

Critical Illness Cover

This add-on benefit offers a lump sum payment upon diagnosis of covered critical illnesses. Now, it includes coverage for up to 64 types of critical illnesses. Additionally, we offer an extended coverage period of up to 85 years to ensure long-term financial support for treatment and recovery.

...Read More

Maternity Cover

With maternity cover, we offer claims for medical expenses during pregnancy and childbirth, such as pre and postnatal care, delivery charges, and even newborn baby coverage.

...Read More

Personal Accident Cover

By taking a personal accident cover, you can get coverage against disability, accidental injuries, and accidental death. This is extremely helpful to safeguard the financial condition of your family in case of unforeseen events.

...Read More

Adding these optional riders to your health insurance plan can enhance its coverage and ensure comprehensive financial protection during medical emergencies.

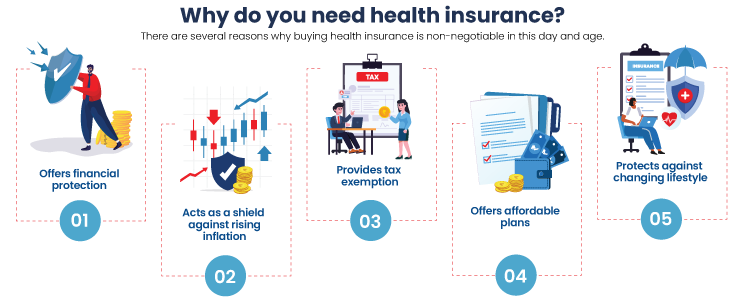

Why do you need Medical Insurance

There are several reasons why buying health insurance is non-negotiable in this day and age -

Offers financial protection

As we already know, medical emergencies can strike without notice. In times like these, it is important to have a fallback for financial protection, since illnesses like cancer, heart ailments, or lung diseases can impact your financial standing. Having a health insurance plan with adequate financial coverage that offers cashless treatment at a wide range of network hospitals is your best bet.

...Read More

Acts as a shield against rising inflation

Beating inflation is hardly possible but its impact can be minimised, particularly by making choices like buying health insurance. It helps individuals meet medical costs in times of emergencies, ranging from the cost of equipment, cost of treatment, medicines and diagnostic tests.

...Read More

Provides tax exemption

Health insurance is also a great way to claim tax deduction up to Rs 25,000 under Section 80D of the Income Tax Act6, on the premium paid towards a policy. Deductions can also be claimed for your spouse or children.

...Read More

Offers affordable plans

Buying health insurance is a necessity today to minimise the impact of rising healthcare costs. It’s a good idea to invest in health insurance early on, because the premium amount will be far lower than when you are older. Also, younger policyholders do not have to go for health check-ups to get the insurance.

...Read More

Protects against changing lifestyle

The lifestyle we lead today is a breeding ground for health issues like diabetes, heart and kidney disorders. That’s why it is important to secure your health beforehand with a comprehensive health insurance plan.

...Read More

How to Choose the Best Health Insurance Plan in India?

Choosing the best health insurance policy requires careful consideration of several factors. You can select the most suitable plan for your healthcare needs by taking care of the below-mentioned points:

Assess Your Healthcare Needs

Determine your healthcare requirements and identify the coverage you need. Consider factors such as age, pre-existing conditions, family medical records, and any specific medical needs.

...Read More

Sum Insured

Evaluate the sum insured offered by different health insurance plans. Ensure that the sum insured is adequate to cover your medical expenses.

...Read More

Network Hospitals

Check the list of network hospitals associated with the health insurance provider. Make sure that the network hospitals are reputable and easily accessible.

...Read More

Coverage and Benefits

Compare the coverage and benefits offered by different health insurance plans. Look for comprehensive coverage, including hospitalisation expenses, pre and post-hospitalisation coverage, outpatient treatments, and coverage for critical illnesses.

...Read More

Premiums and Deductibles

Consider the premium amount and deductibles associated with the health insurance plans. Choose a plan that offers a balance between affordable premiums and comprehensive coverage.

...Read More

Policy Terms and Conditions

Read and understand the terms and conditions of the health insurance plan, including waiting periods, exclusions, and claim settlement procedures.

...Read More

How to Purchase Health Insurance in India?

At this point, hopefully, you have understood the requirements of purchasing a health insurance policy. Here are the steps to purchase health insurance in India:

Know Your Healthcare Needs

Before you choose a particular health insurance plan, you need to estimate the required coverage amount for the insured members of your family.

...Read More

Go to the Insurer’s Website

Visit the Insurer's official website and check the available health insurance plans.

...Read More

Choose the Right Plan

Now, compare and choose among different health insurance plans based on your coverage requirements, affordability and required coverage’s.

...Read More

Understand Policy Terms

It is always recommended to read and understand the policy terms of your chosen health insurance plan to make hassle-free claims in the future. Check the policy terms, conditions, and exclusions before making a purchase decision.

...Read More

Seek Expert advice

In case you are confused about selecting the correct one, you may contact an insurance agent or advisor to get personalised guidance. Even if you are unable to understand the terms, you can ask them for clarification.

...Read More

Apply Online or Offline

You can apply both online and offline for a health insurance plan. You can buy insurance from the agents or directly from the health insurance company. To enjoy a hassle-free process, you need to properly submit the required documents, such as ID proof, address proof, etc., of all the covered members.

...Read More

Make Payment

Pay your health insurance premium at your convenience through offline or online payment methods.

...Read More

Wait to Receive the Policy

The insurance company will complete the verification of the submitted documents. Then, you will receive your policy documents via email ID or by post once your application is accepted. In this document, you will get every detail of your health insurance policy.

...Read More

How to Buy an Online Health Insurance Plan?

After the introduction of online platforms for health insurance, these plans have become more accessible and convenient. Whether you're residing in your home country or abroad, health insurance for NRI individuals is now easy to purchase online. You can buy health insurance online by following these steps:

Research

You should visit the websites of different health insurance companies to compare the premiums and the included benefits. With an online premium calculator, you can do it very easily. By entering your health status, age, required coverage and other details, you get an estimated idea of your health insurance plan.

...Read More

Customise Your Plan

You can customise your health insurance by choosing coverage options to fulfil your unique requirements. Based on your lifestyle and medical history, you need to select an appropriate sum insured.

...Read More

Provide Accurate Information

To avoid claim rejections, you should provide up-to-date and accurate information to your health insurer. For example, your medical history, personal details or any other information related to your medical conditions.

...Read More

Make Online Payment

For online health insurance plans, you need to pay the premium only through online payment methods. Some common options are credit/debit cards, net banking, or UPI.

...Read More

Verify and Receive Policy

You will receive your policy documents as soon as the insurer verifies your details via email.

...Read More

Purchasing health insurance online is a seamless and time-efficient process, offering convenience and transparency throughout.

Who Should Buy Health Insurance Plans?

Here is an overview of who should consider purchasing health insurance, incorporating critical illness and cancer coverage, as well as tax-saving tips.

Young Individuals

By starting early, you get to pay lower premiums to get health insurance. This safeguards you from unexpected medical expenses that can lead to massive expenses.

...Read More

Families

Families can get benefits from health insurance policies designed to cover all members. Family floater plans ensure that everyone’s healthcare needs are covered under a single health premium. If your health insurance has critical illness coverage, it can be beneficial for families with a history of genetic diseases.

...Read More

Self-Employed and Entrepreneurs

For self-employed individuals, health insurance acts as a crucial safety net. It ensures timely access to healthcare services without affecting business finances due to unexpected medical costs.

...Read More

Senior Citizens

As you age, the chances of health issues increase. Health insurance for senior citizens includes coverage for pre-existing conditions, hospitalisations, and critical illnesses.

...Read More

Employees

Many organisations offer health insurance as part of employment benefits. With additional health insurance, you can get better coverage and continuous coverage even if you change your company. You can also get tax benefits under Section 80D of the Income Tax Act6 in India.

...Read More

Individuals Planning for Parenthood

Before you and your partner start to plan for a baby, you can take maternity health insurance. These policies cover pre and post-natal expenses, which helps reduce the financial burden of childbirth.

...Read More

Considering the escalating medical costs and the uncertainties of life, it is prudent for individuals from all walks of life to invest in health insurance plans for financial security and peace of mind.

Factors Affecting Your Health Insurance Premium

Here are the key factors that affect the health insurance premium amount:

Age

Medical History

Lifestyle Habits

Coverage

Geographical Location

Add-On Riders

No Claim Bonus

Younger individuals generally need to pay lower premiums compared to older individuals. As their age increases, the chances of health issues increase and lead to higher premiums.

If you have any pre-existing diseases, your health insurance premium will be higher as there are higher chances of getting ill.

If you are an active smoker or work in hazardous occupations, your health insurance premium will be costly. Bad lifestyle habits need to be disclosed to your insurance provider to avoid claim rejections.

The coverage amount of your health insurance directly affects your premium amount. If you want a higher coverage, you have to pay a higher amount and vice versa.

The medical expense in an urban area is generally higher compared to the rural areas. Therefore, if you stay in an urban area, your health insurance cost will be higher.

If you choose add-on rider benefits such as critical illness, maternity benefits, etc., your total premium amount will increase accordingly.

A no-claim bonus is a reward for you if you do not file claims in a particular year. From 2nd year onwards, you can get discounts on premiums for policy renewals if you have zero claims. Alternatively, your health insurer may offer an increase in the sum insured amount for every claim-free year.

What Is the Cost and Coverage of Health Insurance in India?

When purchasing a health insurance policy, you will want to do a cost-to-coverage analysis to under the benefits offered for the price. Different plans will cater to diverse needs. The premium costs and coverage depend on factors like age, health condition, chosen coverage options, and sum insured.

By evaluating these factors, you can select a health insurance plan that strikes the right balance between affordability and the coverage you are looking for.

What Does a Health Insurance Plan Cover?

A majority of the health insurance plans in India cover the medical expenses given below:

In-patient Hospital Cost

If a patient is hospitalised for more than 24 hours, the insurance plan covers the medical expenses incurred during the treatment of an injury or an illness.

Pre-existing Illnesses or Diseases

Once the waiting period is over, health insurance gives you the option of filing a claim on the expenses undertaken for the treatment of a pre-existing disease or illness.

Expenses before and after hospitalisation

Expenses incurred for medical check-ups, x-rays, and blood tests before hospitalisation, and medicines necessary for smooth recovery are covered under health insurance plans.

Ambulance Charges

Many health insurance plans also cover the expenses incurred for emergency ambulance services. However, the amount covered differs from insurer to insurer.

Maternity Cover

Expenses associated with pregnancy, delivery and newborn care are also covered by health insurance plans in India.

Preventive Health Check-ups

Most health insurance plans in India also cover regular health check-ups to promote regular health checks and timely detection of illnesses.

Procedures for Daycare

Treatments that take less than 24 hours and do not require hospitalisation are also covered by health care policies. These include dialysis, eye surgery, and other daycare surgeries that are mentioned in your health insurance policy.

Home Treatment Cover

For patients who have been advised by their medical practitioner to seek home treatments, health insurance also covers expenses incurred on such healthcare.

AYUSH Benefit

Many health insurance plans cover the expenses incurred on treatments like Homeopathy, Yoga, Siddha, Unani, or Ayurveda.

Mental Healthcare Cover

A health insurance policy in India covers mental health illnesses under the Mental Healthcare Act of 2017. They cover illnesses like schizophrenia, acute depression, bipolar affective disorder, etc.

What Does a Health Insurance Plan Not Cover?

Given below are some of the health insurance exclusions in India:

Insurance claims that arise as a result of injuries due to adventure sports.

You are not eligible to file for an insurance claim for healthcare expenses occurring within 30 days of buying the insurance plans unless an accidental emergency occurs.

Diagnostic tests are not covered.

Health insurance coverage for pre-existing diseases has a waiting period of two to four years.

Rehabilitation and bed rest.

Coverage for critical illnesses has a waiting period of 90 days.

Non-accidental dental procedures.

Injuries caused by nuclear activity, terrorism, or war.

Hormone replacement surgery and cosmetic surgery.

Terminal or chronic illnesses.

Suicide attempts or injuries that are self-inflicted.

Do Health Insurance Plans Cover COVID-19 Claims?

COVID-197 claims are covered under health insurance subject to the following conditions:

1. The patient has valid and ongoing health insurance at the time of hospitalisation9.

2. Minimum 24-hour hospitalisation9 at government-accredited hospitals or hospitals permitted by ICMR.

Note: Other policy-specific conditions might exist and these conditions are subjective. So every individual must check the terms and conditions of their policy thoroughly to know if COVID-197 claims are covered.

What Are the Eligibility Criteria for a Health Insurance Plan?

To avail a health insurance policy from HDFC Life, the minimum age eligibility is typically 18 years, while the maximum age eligibility can vary based on the chosen plan. While pre-existing conditions may be considered, coverage for them may be subject to waiting periods.

Eligibility Criteria |

Specifications |

Age (Adults) |

18-65 years |

Age (Children) |

90 days – 25 years |

Pre-medical screenings |

Depending on the insurer |

Pre-existing diseases |

Waiting period of at least 2 years, depends on the insurer |

Why are many policyholders not fully insured?

- It is not uncommon to find most policyholders buying insurance only so they can save some taxes. However, they fail to understand that the true purpose of insurance is to lend you security during difficult times when you may get financially strained. Saving tax is just an additional or supplementary benefit.

- Therefore, even though numerous insurance products are available in the market today, you must do thorough research to opt for the ones that meet your financial needs well. When this kind of detailed research is not done, one is bound to end up with insurance products that are inadequate despite high premiums.

Why Should You Buy a Health Insurance Plan at an Early Age?

As soon as an individual turns 18 years old, it becomes essential to consider purchasing a health insurance plan.

- Lower Premiums: Purchasing a health insurance plan at an early age enables you to access lower premiums. Younger individuals typically have fewer health issues and are considered less risky by insurance providers, resulting in lower premium costs.

- Comprehensive Coverage: Buying health insurance early ensures that you have a comprehensive coverage plan in place. This safeguards you from unexpected medical expenses, hospitalisation, surgeries, and critical illnesses.

- Financial Preparedness: Life is uncertain, and health-related emergencies can occur at any age. By purchasing health insurance early, you can financially prepare yourself to handle unforeseen medical expenses and protect your savings.

- Coverage Continuity: With age, the chances of developing health conditions increase. By opting for health insurance early, you can ensure continuity of coverage, even if you develop health issues later.

- Pre-existing Condition Waiting Period: Health insurance plans usually have waiting periods for pre-existing conditions. By purchasing a policy early, you can complete the waiting period and avail coverage for any existing health conditions in the future.

Health insurance is a vital investment that provides peace of mind and safeguards your financial well-being. By purchasing a health plan as soon as you turn 18, you secure access to comprehensive coverage, lower premiums, and enhanced protection against unforeseen medical expenses.

What Is the Procedure for Health Insurance Claims?

These are the steps to claim health insurance:

Visit your insurer's website or branch office.

...Read More

Present all the required documents such as hospital bills, medical reports, prescriptions, etc., and fill up the claim form.

...Read More

Once verified, your insurer will pay you the amount.

...Read More

What Documents Are Required to Buy a Health Insurance Plan in India?

To purchase a health insurance plan, you would need to provide documents such as age proof, identity proof, address proof and other KYC documents as per the regulatory requirements. The specific documents may vary depending on your chosen plan and circumstances.

Here are some documents required by most insurers:

- Age Proof: Birth certificate, voter ID card, PAN card or Aadhaar card

- Identity Proof: Voter ID card, Aadhaar card, passport, driving licence or PAN card

- Address Proof: Aadhaar card, voter ID card, ration card, driving licence or utility bills (telephone, water or electricity bills)

- Passport size photographs

- Medical reports: For pre-medical checkups

How Can One Choose the Best Health Insurance Plan in 2025?

To choose the best health insurance plan in 2025, you need to consider coverage options like hospitalisation, outpatient services, and critical illness benefits. You should prioritise health insurance companies with a high claim settlement ratio (CSR) of at least above 90%.

You can check if the premiums are justified against the coverage amount, co-payments and waiting periods. For a smooth claim settlement process, check the insurer's network hospital list.

Why Should You Compare Health Insurance Plans Online?

Comparing health insurance plans online is essential to make an informed decision. Some reasons why you should compare health insurance plans online are:

Convenience

Comparing health insurance plans online allows you to do a cost/benefit analysis of various policies from different insurance providers. You can review the coverage, benefits, premiums, and other policy details without leaving your home.

...Read More

Wide Range of Options

Online platforms provide a wide range of health insurance options from different insurers. You can compare multiple plans side by side and choose the one that best fits your requirements.

...Read More

Cost-Effective

Online comparison platforms often offer exclusive deals and discounts. By comparing health insurance plans online, you can find cost-effective options that provide comprehensive coverage.

...Read More

Real-Time Quotes

Online comparison platforms provide real-time quotes, allowing you to see the premium amounts for different health insurance plans instantly. This helps in making quick comparisons and decisions.

...Read More

Transparent Information

Online platforms provide detailed information about each health insurance plan, including coverage, benefits, exclusions, and policy terms and conditions. This transparency helps you make an informed choice.

...Read More

How to Calculate Health Insurance Premium?

Health insurance premium calculation is based on several factors, including:

- Age: Premiums generally increase with age as the risk of medical conditions and complications increases.

- Sum Insured: A higher sum insured leads to a higher premium.

- Medical History: Existing medical conditions and medical history of the insured can impact the premium amount.

- Lifestyle Habits: Certain lifestyle habits like smoking, drinking alcohol, and lack of physical activity may result in higher premiums.

- Policy Type: The type of health insurance plan and coverage options chosen can also impact the premium amount.

- Family Coverage: If you opt for a family health insurance plan that covers multiple family members, the premium will be higher.

What Is a Mediclaim Policy?

Mediclaim policies provide financial coverage for hospitalisation expenses such as room charges and treatment costs. It is a comprehensive health insurance plan that covers AYUSH treatments, modern treatments, etc.

It requires hospitalisation to claim the benefits and does not allow customisation or family coverage. To make a claim, you need to submit proof of expenses like hospital bills for reimbursement.

Difference Between Mediclaim and Health Insurance

Check this table to learn the difference between mediclaim and health insurance:

Factor |

Mediclaim |

Health Insurance |

Coverage offered |

In mediclaim, you can only get compensated for hospitalisation expenses. |

With hospitalisation, you can also get pre- and post-hospitalisation expenses, ambulance expenditures, OPD costs, etc. |

Sum Insured |

The maximum amount of sum insured is generally Rs. 5 lakh. |

Nowadays, you can even get up to 1 crore of health insurance. Further, you can even increase it with a top-up or super top-up health insurance plan. |

Add-on Covers |

There are no options to get any add-on cover or rider benefits with mediclaim. |

With most health insurance plans, you can get multiple add-ons such as personal accident, critical illness, maternity cover, etc. |

Customisation |

It is difficult to customise your health insurance to meet your specific needs. |

With health insurance, you can easily make customisations to meet your unique requirements. |

What Is the Difference between Health Insurance Plan, Cancer Insurance, and Critical Illness Insurance?

While health insurance plans, cancer insurance, and critical illness insurance provide coverage for medical expenses, there are some key differences:

|

Cancer Insurance |

Critical Illness Insurance |

Health Insurance Plans |

|---|---|---|---|

Reason to purchase the insurance |

It is a benefit-based policy that pays a lump sum after diagnosis to cover the cost of cancer treatment. |

It is a benefit-based policy that pays a lump sum after diagnosis. |

It is an indemnity-based policy that covers the expenses incurred for treatment or provides the option of cashless treatment. |

What does the insurance cover? |

The policy provides coverage for costs incurred at every stage of Cancer. |

It covers expenses incurred on critical illnesses that are mentioned in the policy document. |

Covers the expenses incurred on treatments and surgeries. |

Who should purchase the insurance? |

A cancer insurance can be purchases along with a health insurance plan. It is ideal for individuals who want to be prepared against cancer. |

A critical illness insurance can be purchases along with a health insurance plan. It is ideal for individuals who want to be prepared against critical illnesses. |

Health insurance plans are ideal for covering the increasing healthcare costs. |

Health Insurance Plan

A health insurance plan covers a wide range of medical expenses, including hospitalisation costs, doctor's fees, medications, and surgeries. It provides financial coverage against various illnesses and medical emergencies up to a limit called the sum insured.

...Read More

Cancer Insurance

Cancer insurance is a specific type of insurance that focuses on providing coverage for cancer-related treatment and expenses. It offers a lump sum payout upon the diagnosis of cancer, which can be used for medical treatment, supportive care, and other necessities.

...Read More

Critical Illness Insurance

Critical illness insurance covers life-threatening illnesses such as heart disease, stroke, organ failure, and major surgeries. It provides a lump sum benefit upon the diagnosis of a covered critical illness, which can be used for medical treatment, recovery, and financial obligations.

...Read More

While health insurance plans provide comprehensive coverage for a wide range of medical expenses, cancer insurance and critical illness insurance offer specialised coverage for specific illnesses. However, they usually provide a higher sum insured.

Ensure Protection against Medical Emergencies with Health Insurance

Health insurance provides vital protection against medical emergencies, ensuring financial security and peace of mind. With rising healthcare costs, it is crucial to have a comprehensive health insurance plan in place.

HDFC Life offers a range of health insurance plans that offer extensive coverage and benefits, enabling individuals and families to access quality healthcare without worrying about the financial burden.

How to Obtain a Physical Copy of Your Health Insurance Policy?

Follow the steps mentioned below to get the physical copy of your health insurance policy

Visit the branch of your insurer and get in touch with an executive there.

...Read More

You will be given a form to fill, complete all the details required to be filed in it, such as your name, policy name, and policy number. Remember to fill in your registered address as well.

...Read More

Give a verbal or written request to send the physical copy of your policy to the address shared.

...Read More

The above step may vary depending on company process.

How to get a copy of your health insurance policy online?

Here are the steps to be followed to get a copy of your health insurance policy online:

- Step 1 : Login into your Account with using your ID and password..

- Step 2 : Once you have access to your account, you can go to the policies section.

- Step 3 : Select ‘download’ for the policy whose copy you want.

- Step 4 : Once downloaded, you can take a printout of the document for keepsake. You can also store it electronically on your laptop or mobile device.

The above step may vary depending on company process.

Steps to Renew Your Health Insurance Online

You can easily renew your health insurance online by following the steps given below:

- Step 1 : In most cases, you will receive a policy renewal email with a link to your policy renewal page. Simply enter your password to access and follow through. You can go ahead and make a quick and secure payment via net banking or any of the UPI apps of your choice.

- Step 2 : Alternatively, you can visit the insurers website and log into your account. Now select the policy you want to renew and make a quick and easy payment via net banking or any of the UPI apps of your choice.

- Step 3 : Once the payment is made, you can expect to get an email confirmation regarding the same and a renewed policy document as well.

The above step may vary depending on company process.

Myths about Health Insurance

There are several myths surrounding health insurance that need to be addressed:

1 Myth#1 Health insurance is only for the elderly.

Fact: Health insurance is beneficial for individuals of all ages. It provides financial protection against medical emergencies and ensures access to quality healthcare.

2 Myth#2: Health insurance covers all medical expenses.

Fact: While health insurance covers a wide range of medical expenses, there are certain exclusions and limitations. It is essential to read and understand the policy terms and conditions to know the coverage details.

3 Myth#3: Health insurance is expensive.

Fact: Health insurance premiums vary based on factors such as age, sum insured, and coverage options chosen. With careful comparison and selection, affordable health insurance plans can be found.

4 Myth#4: Buying health insurance means unnecessary expenses.

Fact: Health insurance provides financial protection during medical emergencies. It helps in avoiding heavy out-of-pocket expenses and ensures access to quality healthcare.

5 Myth#5: Health insurance is unnecessary if I am young and healthy.

Fact: Medical emergencies can happen to anyone, regardless of age or health condition. Having health insurance provides financial security and peace of mind for unforeseen medical events.

To Sum Up

Health insurance is designed to help you manage your medical bills and obtain timely care without breaking the bank. In addition, complementing it, with a life insurance provides your loved ones with long-term financial protection, allowing them to retain stability in the face of unanticipated situations. Together, these plans provide a balanced approach to financial readiness and peace of mind for you and your family.

FAQs on Health Insurance Plans

1 Which is the best health insurance in India?

The best health insurance policy in India depends on individual requirements, coverage needs, and budget. It is recommended to compare different health insurance plans to find the one that suits your needs.

2 How can I get health insurance?

Health insurance can be purchased directly from insurance companies or through insurance agents.

3 How do I choose a health insurance plan?

Choose a health insurance plan based on factors such as coverage, benefits, premium affordability, network hospitals, and policy terms and conditions.

4 What are the diseases covered under the health insurance policy?

The diseases covered under a health insurance policy may vary depending on the plan and insurance provider. Commonly covered diseases include cancer, heart disease, kidney-related ailments, and others.

5 Which health insurance plan covers cancer?

Cancer insurance plans provide specific coverage for cancer-related treatments, including chemotherapy, surgery, and supportive care.

6 How soon can I use my health insurance policy?

The waiting period for health insurance policies varies. Read the policy terms and conditions to know when the coverage begins.

7 Do normal health insurance plans cover critical illness?

Normal health insurance plans may not cover critical illnesses. However, critical illness insurance policies and riders provide coverage for life-threatening illnesses.

8 Is it better to take a critical illness policy or health insurance plan?

Critical illness insurance and regular health insurance plans serve different purposes. A combination of both provides comprehensive coverage.

9 How much does health insurance cost for an individual?

Health insurance costs for individuals depend on factors such as age, sum insured, coverage, policy terms, etc.

10 What are the documents required for buying a health insurance plan?

The documents required for buying a health insurance plan include identity proof, address proof, age proof, and some additional documents as per the insurer's requirements.

11 How do I estimate the cost of health insurance?

The cost of health insurance can be estimated by comparing premiums, coverage, and benefits offered by different insurance providers.

12 What is the right time to buy a Health Insurance Plan?

It is advisable to buy health insurance at a young age to avail lower premiums and ensure early coverage.

13 What are the maximum and minimum health insurance policy duration?

The maximum and minimum health insurance policy durations vary across insurance providers and policy types. It is best to check with the insurer for specific details.

14 What is the limit for 80D medical insurance premiums?

According to section 80D of the Income Tax Act of 1961, individuals can claim a deduction of up to Rs 1,00,000 on the health insurance premium they pay.

15 Can I claim from 2 health insurance policies?

Yes, you can split the cost of medical expenses incurred between two policies as long as the total amount does not exceed the actual expenses.

16 What is the best medical insurance?

The best health insurance is the one that offers the maximum coverage, has a network of hospital tie-ups, and provides cashless claims with affordable premiums. On the whole, the best plan is one that meets your needs, including pre-and post-hospitalisation expenses and critical illnesses. Check whether your plan features riders for additional coverage.

17 How many types of health insurance are there in India?

There are many different types of health insurance plans in India, including Individual health insurance plans, Family Floaters, Critical Illness Plans, Riders and Top-up Plans, Senior Citizen Plans and also, Group Insurance Plans.

Related Articles to Health Insurance

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance solutions - protection, pension, savings, investment, annuity and health.

Buy Health Insurance in Other Cities

- Health Insurance in Mumbai

- Health Insurance in Delhi

- Health Insurance in Hyderabad

- Health Insurance in Bangalore

- Health Insurance in Kerala

- Health Insurance in Chennai

- Health Insurance in Aurangabad

- Health Insurance in Chandigarh

- Health Insurance in Kochi

- Health Insurance in Tamil Nadu

- What is Health Insurance

Popular Searches

- term insurance

- Health Insurance Plans

- What is Health Insurance

- Benefits of Health Plans

- BMI Calculator

- Human Life Value Calculator

- Savings Plans

- ULIP Plans

- Group Insurance Plans

- Child Insurance Plans

- Pension Calculator

- ULIP for Health Benefits

- Compound Interest Calculator

- Easy Health Plan

- How to Choose Best Child Insurance Plan

- Fixed Maturity Plan

- ULIP Vs SIP

- Financial Planning for your 50s

- Zero Cost Term Insurance

- critical illness insurance

- Whole Life Insurance

- types of term insurance

- Benefits of Life Insurance

- Endowment Policy

- child savings plan

- life insurance

- life insurance policy

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- Saving Schemes

- Health Insurance of smokers

- Health Insurance of Self employed

- Types of health insurance

- Health Insurance for Women

- 2 Lakh Health Insurance

- 10 Lakh Health Insurance

- 3 Lakh Health Insurance

- Best Term Insurance Plan for 1 Crore

- features of term insurance

- personal accident insurance

1. Annual Premium amount ₹ 1869 for Male aged 35 years, Base Benefit, 10 years term, Regular Pay option, Sum Assured=10 lakhs, excluding Taxes & levies as applicable.

6. As per Income Tax Act, 1961. Tax benefits are subject to changes in tax laws.

7. Option available under COVID-19 health cover.

9. On positive diagnosis of COVID-19 in a Government authorized diagnostic centre as per terms and conditions.

ARN- DM/01/25/20084