- Webpages

- Documents

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

-

![login]() Customers

Customers

-

![login]() Employees

Employees

-

![login]() Partner

Partner

- Consultants

- Partner Portal-FC

For NRI Customers

(To Buy a Policy)

-

![Contact Image]()

Call (All Days, Local charges apply)

-

![Contact Image]()

Email ID

-

![Contact Image]()

Whatsapp

(If you're our existing customer)

-

![Contact Image]()

Call (Mon-Sat, 10am-9pm IST, Local Charges Apply)

-

![Contact Image]()

Email ID

For Online Policy Purchase

(New and Ongoing Applications)

-

![Contact Image]()

Call (All Days & Toll free)

-

![Contact Image]()

Schedule a call

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Give missed call to buy a policy

-

![Contact Image]()

Email

Branch Locator

-

![Contact Image]()

Locate a branch

For Existing Customers

(Issued Policy)

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Call (Mon to Sat, from 10 am to 7 pm, Call charges apply)

-

![Contact Image]()

Email

Fund Performance Check

-

![Contact Image]()

Call (Missed Call)

We at HDFC Life are committed to maintaining the highest level of customer service. Hence we have tried to provide you with all the information you may want to seek regarding customer support, value added services, and various policy servicing options. We are also seek feedback on our products and services that will help us to serve you better.

1 Customer Support

HDFC Life has a skilled and dedicated centralized operations team to support end to end customer service requirements of corporate clients.

The team provides servicing support to process customer service requests and query resolution while maintaining high standards of quality.

Group Operations Team can be reached basis the policy availed from HDFC Life:

Group Term Insurance (GTI) @ [email protected]

Credit Protect (CP) @ [email protected]

Group Unit Linked Plan @ [email protected]

1 Go Green

Go Green is an HDFC Life initiative that promotes environmental values towards saving the planet. Going green looks and feels right, plain and simple.

Benefits of the Go Green

- Save the Earth

- Enhanced turnaround time

- Paperless transactions

- Easy and faster retrieval of data

- Tamper proof data

Services offered under Go Green

- Electronic Pay-out : This facility helps the insurer to transfer funds into policyholders account through RTGS or NEFT

- Digitally signed communication: a document which is digitally signed authenticates the identity of the person and ensures that original content of the document is unchanged.

- Registered E-mail ID : This facility allows the trustees / policyholder to send scanned image of signed documents through authorized email id’s and hard copy instructions can be waived off.

To sign up and assist in our Go Green objective please fill the, attached form

1 Funding Business (ULIP/ Traditional)

What details / documents are required for Additional Contribution request received for funding – Unit Linked and Non Unit Linked Plans?

The following details / documents are required for Additional Contribution request received for funding business (Unit Linked and Non Unit Linked Plans):

A. For Additional Contribution DB (Defined Benefit):

- Duly filled Contribution form with authorised trustee signature and trust stamp on the contribution form.

- Fund Transfer details along with UTRN/Bank details/PIS details in case of cheque.

B. For Additional Contribution DC (Defined Contribution):

- Duly filled Contribution form with trustee signature and trust stamp on the contribution form

- Fund Transfer details along with UTRN/Bank details/PIS details in case of cheque

- Member annexure form with Contribution details.

Please note as per IRDA notification dated 26th of July 2019 viz. IRDAI (Non Linked Insurance Products) Regulations, 2019 and IRDAI (Unit Linked Insurance Products) 2019, written consent has to obtain from the client to continue and adding new members under the existing Group Variable plan (GVIP).

As per the new IRDAI CIRCULAR (IRDA/Act/GDL/PRD/135/06/2012) dated 13th June 2012, no new members can be enrolled in the superannuation Schemes launched prior to 28/Mar/13.

Which are the documents required for Merger of the Trust?

The documents below are required for merger of the Trust (cases where policies of both the Trust are maintained with HDFC Life):

- Documents of the policy to be surrendered (Claim form and Policy documents).

- Copy of Board Resolution.

- Acknowledgement copy of request letter sent to Commissioner of Income Tax (CIT) for approval.

- Copy of Court Order.

- Letter from the client to transfer funds from surrendered policy and move the proceeds to another policy. (Common letter will suffice if the Trustees are same for both the policies)

- PAN card of any one of authorized signatories attested with Trust stamp and signed by authorities

Note: Policy will be surrendered on T Day and New Business will be set up on T+1 day subject to cut off norms.

All the above documents need to be attested by the Trust and signed by the Trustees.

What is the validity of a cheque issued?

As per RBI guidelines with effect from 1 April' 2012, all cheques/Demand Drafts/Pay orders with mentioned dated 01/04/2012 will be valid for 3 Months from the date of issue.

Would it be possible to include the new members in the existing Superannuation policy?

As per the new IRDAI CIRCULAR (IRDA/Act/GDL/PRD/135/06/2012) dated 13th June 2012, no new members can be enrolled in the superannuation Schemes launched prior to 28/Mar/13.

Further as per the IRDA notification dated 26th of July 2019 viz. IRDAI (Non Linked Insurance Products) Regulations, 2019 and IRDAI (Unit Linked Insurance Products) 2019, written consent has to be obtained from the client to continue and adding new members under the existing Group Variable plan (GVIP).

Which modes of request can help us avoid physical policy servicing for form transitions?

Hard copies for the policy servicing request are not required in case the request is received through:

- Registered Email ID

- Group Portal

- Indemnity Mandate signed

Can fund switch and premium redirection request be processed on the same day for a particular policy?

Yes, fund switch and premium redirection can be processed on the same day for a particular policy, wherein fund switch is processed first followed by premium redirection request.

Note: Contribution cannot be processed along with this transaction.

Which documents/details are required for NEFT service?

Complete NEFT mandate form duly signed by authorised signatories and attested with Policy holders stamp to be sent along with the following: Cancelled cheque (with IFSC, Bank account number & name of the client trust)

OR

Bank official stamp and sign on the NEFT mandate form with account number, name of client trust and IFSC details without any overwriting.

What are the check points while sending the NEFT mandate?

Following are the check points while sending across the NEFT mandate:

- Cancelled cheque copy to be sent along with the duly filled mandate form.

- The details mentioned in the mandate should tally with the cancelled cheque copy such as IFSC, account type (saving / current) and account number.

- The mandate to be duly signed by authorised signatory and attested by a trust stamp.

- Wherein cancel copy of cheque is not available, Bank official stamp and sign on the NEFT mandate form with account number, name of client trust and IFSC code details without any overwriting.

What is the procedure for surrendering the existing policy and transferring the Corpus to the new policy with HDFC Life?

For surrendering the existing policy and transferring the Corpus to the new policy with HDFC Life, below documents are required:

- Surrender letter mentioning the reason for surrender signed by the authorised signatories.

- Original policy document from the Client.

- Documents for setting the new policy.

- In case if there are no changes in the existing board resolution, Trust deed and rules, then a letter stating the same to be provided by the Trustees.

- Policy to be surrendered on T Day and New Business to be set up on T+1 day subject to cut off norms.

- PAN card of any one of authorized signatories attested with Trust stamp and signed by authorities

What if the Trust does not have a Pan Card?

PAN Card details are mandatory for premium equal to or above ₹ 50,000. If the Trust does not have a PAN Card, then the Trust needs to apply for PAN Card / provide us with Form 60 or 49 A with every contribution.

Would a signed scanned copy of policy servicing form be mandatory for Funding Business?

Funding: The signed scanned copies of the policy servicing forms to be provided for funding Business (GULP / Group Traditional Plan set up for Gratuity / Pension / Leave Encashment schemes) if the request is received through registered email ID. Please note soft copies of member information form / account information form for SA DC clients is required to initiate the request.

Can Transaction wise statement be provided in Superannuation DC Schemes?

Transaction wise statements can be provided to Superannuation DC clients in following scenarios:

- Either on policy anniversary or 31st of March.

- Transaction wise statement can be provided to the members if request is received through portal.

- If the transaction wise statement request is received through email mode (more than once, which includes below scenarios).

- The member would be charged ₹ 100 or ₹ 50 wherein already Group Portal Facility is provided. Please check policy details for exact applicable charges.

- Transaction wise statement for Superannuation DB clients is non-chargeable.

- Member wise /Group wise Fund statement can be provided to the clients which is non-chargeable for new products (GVIP, Par Pension, New Gulp Pension).

Which are the documents required for surrendering the policy?

The documents required for surrendering the policy are as follows:

- Surrender letter mentioning the reason for surrender signed by authorised signatories.

- Original policy document from the Client.

Which are the documents required for Change in Trust name?

The below documents are required from the client for Change in Trust name:

- Board Resolution

- Trust Resolution stating the name change

- Change in Trust name letter

- Bank Particulars

- Attested copy of Pan card with the new trust name

- Trust Stamp and Trustee signature to be incorporated on all the documents

- Deed of Variation is applicable if required.

Which are the documents required for Change in address of Trust?

The below documents are required from the client for Change in address of Trust :

- Board Resolution

- Trust Resolution stating the address change

- Letter from Trustees of the client mentioning the address change

- Bank Particulars ( incase if any changes in bank details due to change in address of trust)

- All documents has to be attested with Trust Stamp and signed by authorized signatories.

Which documents are required for Change in Trust Name in case of partnership firms and companies?

The following documents are required:

- In case of partnership firms - revised Partnership Deed, PAN Card and Bank Account particulars

- In case of Companies -Resolution passed by the Board, fresh certificate of incorporation, PAN Card and Bank Account particulars

- In case of Trusts - Letter from Trustees, Resolution passed by the Trustees, fresh certificate of incorporation of Employer, PAN Card and Bank Account particulars

- Deed of Variation is applicable if required

Which documents are required for Change or Addition in Trustees?

The following documents are required:

- A Trust resolution stating that the new Trustees have been appointed.

- Trust resolution should state that decisions on behalf of the Trust can be taken by the newly appointed Trustees jointly / severely on behalf of the Trust.

- Specimen Signature of the newly appointed Trustees.

- If all the existing Trustees are resolved then a complete set of new appointed Trustees are required and the same should be signed by the authorised Signatory of the Company. (Chairman/ Company Secretary/ Managing Director)

- PAN Card of any one of authorized signatories attested and signed by authorized signatories.

How many members are at the least required at the time of New Business for the funding products?

Minimum numbers of members required are as follows:

- GULP Pension - 10

- GULP Life - 10

- GVIP - 10

- Traditional Plan - 50

What is the minimum amount of premium required for the New Business of funding products?

Minimum premium amount at New Business are as follows:

- GULP Pension – ₹ 5 Lacs

- GULP Life - ₹ 5 Lacs

- GVIP - ₹ 5 Lacs

- Traditional Plan: There is no specific minimum premium that needs be paid.

- There is no specific maximum premium amount per scheme or per member. However, the company may choose to not accept premiums larger than ₹ 50 Cr if this were not in the wider interests of the fund receiving the investment at that time.

For which products NRA details are required?

NRA details are required for the following products:

- GULP Pension – NRA required for DC schemes

- GULP Life - NA

- GVIP – NRA required for DC schemes

- Traditional Plan - NRA required for DC schemes

For which products DOB details are required?

DOB details are required for the following products:

- GULP Pension – DOB required for DC schemes

- GULP Life - NA

- GVIP – DOB required for DC schemes

- Traditional Plan - DOB required for DC schemes

Whose name should be the cheque received from group clients, be drawn on?

Cheque should be drawn on:-

- HDFC Life Insurance Company Ltd

What are the Fund Transfer details?

Details of Fund transfer within the country are as below:

For Unit Linked policies and Non Unit Linked policies:

Bank Name |

HDFC Bank Ltd. |

Bank Address |

HDFC Bank Ltd. |

Bank A/C No. |

57500000195130 |

A/C Name |

HDFC Life Insurance Co. Ltd. GROUP CONVENTIONAL COLLECTION A/C |

IFSC Code |

HDFC0000060 |

What RCD will be given for New Business / Contribution received in Non unit linked Plan?

Payment received via cheque mode: RCD will be as on cheque clearance date subject to documents being received by 3PM.

Payment received via fund transfer / RTGS: RCD will be subject to funds being received at HDFC Life account by 1.45 pm and available for investment and documents being received by 3PM. (Such transfers to be notified by phone call and email to [email protected] (HDFC Life)

Which are the businesses that have been discontinued effective 1st Aug’13?

Effective 1st Aug’13, following new business has been discontinued:

- Credit Protect - 1 year term

- GVTI - 1 year term

- GULP - Life & Pension - DC schemes

- GULP Option "O" and "N" (both Life DB ) which were open for sale have now been stopped for New Business

- GTP and GCP --- Life and Pension new business as well as new member additions are no longer allowed

- Old Group Traditional

- DIP

- Old Group Variable Employee Plan

2 Non Funding Business (GTI)

Will it be possible to change the employee identification number during the mid year for the Group term insurance policies?

Changes in the employee identification number is permissible during the mid year for Group Term Insurance Policies.

Which are the documents required to change the company name during the policy year for Group Term Insurance policies?

The documents mentioned below are required while changing the company name during the policy year:

- ROC (Certificate of Registration)

- Pan card copy

- Certificate of Incorporation

Cheque payments for Group clients should be drawn on which name?

Cheque should be drawn on:-

- HDFC Life Insurance Company Ltd.

What will be the validity of the issued cheque?

As per RBI guidelines with effect from 1 April' 2012 all the Cheque/Demand Draft/Pay order with mentioned dated 01/04/2012 will be valid for 3 Months from the date of issue.

Who should sign the consent form in case of Extra Premium Charged?

It should be signed by an authorised signatory along with the stamp needed to affix the same.

Are hard copies required for policy servicing requests?

Hard copies for the policy servicing request are not required in case the request is received through:

- Registered Email ID

- Digital ID (System Available with client)

- Group Portal.

- Indemnity Mandate signed

Which policy servicing requests can be allowed under "Email ID Registration" facility for GTI client?

Below are the lists of servicing requests that are allowed under "Email ID Registration" facility:

- Mid Joiner

- Mid Leaver

- Change in Sum Assured

- Alterations

- APS/AML request

- No claim Letter

- Pan card

- Certificate of Registration / Certificate of Incorporation

- Member list - GTI Renewal cases only

- Renewal documentation

- Acceptance of additional premium for rate up by the policyholder

- Declaration of Good Health and Medical Questionnaire (Must be signed by members)

- GST Certificate updation

- Refund/ Lapsation Request

Note: Declaration of Good Health, Medical Questionnaire, Covid Questionnaire, Rate up letter and Renewal documents will be accepted from registered email ID only once it is stamped and signed by an authorised signatory. In order to have signature-free acceptance for the concerned requests at our end, client has to sign an indemnity bond with us.

What details are required for a domestic fund transfer (within India)?

Details of Fund transfer within the country are as below:

For Conventional Product:

| Bank Name | HDFC Bank Ltd. |

| Bank Address | HDFC Bank Ltd. Maneckji Wadia Bldg, Gr Flr Nanik Motwani Marg, Mumbai 400 001. |

| Bank A/C No. | 00600350011825 |

| A/C Name | HDFC Standard Life Insurance Co. Ltd. |

| IFSC Code | HDFC0000060 |

What is the grace period for submission of Renewal documents / Payment of Premium for Group Term Insurance Plan?

A grace period of 15 days for monthly Premium paying frequency and 30 days for other Premium paying frequencies is allowed for the payment of each renewal Premium after the first Premium.

What is the process to lapse the GTI policy?

Client has to send us the Email notification to lapse the policy along with NEFT form & Cancel Cheque duly signed and stamped.

Policy is not renewed from the Last risk cover date, in such case policy will be auto lapsed by system on 181st day from Last Risk Cover Date and funds will be moved to Unclaimed Account.

If the existing GTI client wants to take a new GTI policy with us, will the CIF (Company Information Form) of the existing policy hold good?

New CIF is mandatory for any New Business received irrespective of client having existing policy with us.

What details should be mentioned in the proposal form with regards to maximum age of joining the Group Term Insurance Plan?

Maximum age for members to join the scheme should always be less than 1 year of Normal Retirement age mentioned on the proposal form.

Eg: If the Normal retirement age is 60 yrs then Maximum age should be 59yrs.

Which are the documents required for New Business of GTI policy?

Below is the list of documents for New Business:

- Proposal Form

- Sales Illustration

- Member list

- Premium Quotation

- PAN Card Copy or Pan number of MPH

- PAN Card copy of Authorised Person

- GST Certificate

- Go Green Form/ Standing Instruction

- Premium Payment

- Certificate of Incorporation

Which are the documents required for Renewal GTI policy?

Below is the list of documents for Renewal.

- Sales Illustration

- Member list

- Premium Quotation

- PAN Card Copy to be removed

- Go Green Form/ Standing Instruction

- Premium Payment

What will be the risk commencement date (RCD) for new business?

The risk commencement date (RCD) for new business can be funds received date or date post the funds received subject to the validity of the premium quotation.

Does the Pan Card copy needs to be signed and stamped?

Yes, the Pan Card copy should be duly signed and stamped by the authorised signatory.

3 Credit Protect Plan

What is the Group Insurance and what is the Master Policy Holder?

Group Insurance is a tri-party arrangement where three parties are involved. Master policyholder, Insurer and customer. Master Policy Holder is an institution, bank, NBFC or any other affinity group through which group insurance policy is sourced to their customers. For e.g. in case of loan linked policies, bank or NBFC or any other lending institute becomes the Master Policy Holder whereas borrower is customer and HDFC Life is an insurer.

Do I get any communication post issuance of policy?

Yes, Certificate of Insurance is sent to all our customers immediately post issuance through various modes like Bitly SMS, email etc. Hence we request all our customers to share contact details to enable HDFC Life to keep our customers informed about important policy details.

Does it have tax benefits?

Certificate of Insurance is the proof of premium paid for the policy. Hence you can avail tax benefit showing the Certificate of Insurance.

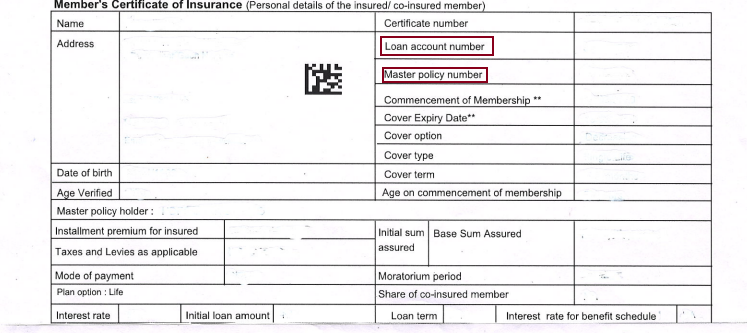

Are there any mandatory details to be shared with HDFC Life to raise any servicing request?

To identify correct policy details and help you better, we request all our customers to share details like master policy number, name of master policyholder & loan account number or any other unique number shared with HDFC Life at the time of issuance of policy.

Can I get a copy of my policy?

HDFC Life is committed to issue Certificate of Insurance (COI) to all their customers immediately post issuance of policy. However if you are not able to trace the COI, then you can raise request with HDFC Life for copy of the same.

You can visit Master policyholder or alternatively you can visit nearest HDFC Life Branch for copy of COI.

How Can I raise request for changing / altering policy details?

You can visit nearest HDFC Life Branch to raise request to change policy details. You need to fill up Group policy servicing form with valid KYC documents.

Alternative, you can fill up attached group policy servicing form and send a request along with valid KYC documents at [email protected]

Kindly use standard subject line as “Alteration Request_LAN No & MPH No.”

Please find below KYC details required for different types of alteration requests (PAN card to be mandatorily shared for all requests):

1. Address change - Address proof

2. Name Change - ID proof, If you are a married woman with a change in surname, please submit a copy of your marriage certificate. For any other request involving significant changes in the name, please submit a 'Gazette Copy'

3. Change in Date of Birth - ID proof

4. Change in registered contact details & email id – ID proof

To identify correct policy details and help you better, we request all our customers to share details like master policy number, name of master policyholder & loan account number or any other unique number shared with HDFC Life at the time of issuance of policy.

What is the Turn Around Time for processing change / alterations requests?

Post receipt of all mandatory documents and information, change requests would be processed within 10 working days.

Do you share any communication post processing alterations / change request?

Yes, we do share endorsement to communicate changes made to initial policy.

Do I get any communication if I need to complete any medical requirements?

Yes, SMS and email communications are sent to all our customers to complete the Underwriting requirements.

What Do I need to do to complete medical & other underwriting requirements?

You need to connect with the Master policyholder to initiate Underwriting process. Full underwriting form is required to initiate the process.

Can I cancel my policy during the freelook period?

As per IRDAI regulations, if you are not satisfied with terms and conditions of the policy, you are entitled to raise request to cancel the policy during free-look period. You have a period of 15 days to review your original policy document from the date of receipt to return it to us for cancellation, and you will be eligible for a refund.

If your policy is sourced through distance marketing, you have a period of 30 days. This will be mentioned in your policy certificate.

Can I surrender the policy if underlying loan is foreclosed?

Yes, you can surrender your group policy post foreclosure of loan.

What is the surrender value payable to me?

Surrender value depends on outstanding term and outstanding sum assured. A table containing Surrender Value at different time during the policy period is shared along with Certificate of Insurance.

How do I raise request for Free look cancellation or surrender of policy?

You can connect with Master policyholder for raising request for cancellation or surrender of policy. Alternatively, you can write to us at [email protected] along with NOC from master policyholder to process cancellation.

Kindly use standard subject line as “Surrender / Freelook in Cancellation Request LAN No____ & MPH No.__”

To identify correct policy details and help you better, we request all our customers to share details like master policy number, name of master policyholder & loan account number or any other unique number shared with HDFC Life at the time of issuance of policy.

What is the Turn Around Time for processing freelook cancellation or surrender requests?

Post receipt of mandatory documents, refund request would be processing within 7 working days and payment details along with UTRN will be shared with you via SMS / Email.

What are the mandatory documents for raising Freelook cancellation or surrender request?

Below documents are mandatory for sharing request with HDFC Life. You can visit nearest HDFC Life Brach or alternatively you can write to us at [email protected]

- Certificate of Insurance (COI)*.

- No Objection Certificate (NOC) from master policyholder.

*If you are not able to trace COI then please share loan account number and master policy number while raising request with HDFC Life.

If you wish to receive the surrender amount in your account, we additionally require below documents:

- Cancelled cheque with preprinted name or NEFT form duly filled, signed & stamped by bank.

<<NEFT mandate form to be attached>>

It is subject to approval from master policyholder.

Do you send any communication post cancellation of policy?

Yes, Payout SMS / Email is sent to all our customer wherever mobile no. & email id is shared with us at the time of issuance.

Can we add multiple nominees under one policy?

Yes, you can add maximum 4 nominees against one policy.

How can you appoint a nominee for your policy?

You may appoint a nominee while submitting the proposal by providing nominee details in the proposal form.

How can you add a nominee if no nominee was appointed at the time of proposal? Can a nominee be added after the policy has been issued?

You can visit nearest HDFC Life Brach to raise request to change policy details. You need to fill up Group policy servicing form with valid KYC documents.

Alternatively, you can fill up attached group policy servicing form and send a request along with valid KYC documents to [email protected]

Please note KYC documents required for addition / modification of nominee (PAN card to be mandatorily shared for all requests)–

- ID & Address proof of Life Assured

- ID & Address proof of Nominee

Can a minor be appointed as a Nominee?

Yes. But when you are appointing a minor as your nominee, you will also have to appoint an appointee.

Who is an appointee?

An appointee may be appointed to receive the policy moneys in case of death of the life assured during the minority of the nominee. The appointee should be a major person.

Can I Add / Change Appointee?

Yes you can add / change appointee. You can visit nearest HDFC Life Brach to raise request to change policy details. You need to fill up Group policy servicing form with valid KYC documents.

Alternatively, you can fill up attached group policy servicing form and send a request along with valid KYC documents to [email protected]

Please note KYC documents required for addition / modification of appointee (PAN card to be mandatorily shared for all requests)–

- ID & Address proof of Life Assured

- ID & Address proof of Appointee

What happens if the nominee dies before the policyholder?

If the nominee dies before the policyholder, new nomination needs to be added to the policy by policyholder. In case if new nomination is not added before the death of Life Assured, then policy proceeds will be payable to legal heirs basis valid documentation.

To add nominee to the existing policy, please refer question - How can you add a nominee if no nominee was appointed at the time of proposal? Can a nominee be added after the policy has been issued?

Can I assign my Group Insurance policy?

No, Group policy cannot be assigned.

If I transfer my loan to any other Finance/ Bank Can I transfer my insurance as well?

No. Group Insurance policy cannot be transferred.

What if death claim intimated prior to issuance policy and COI?

Insurer is responsible to admit claims where COI has been issued to the Life Assured. Any policies where COI is not issued to Life Assured on account any pending requirements; insurer is not responsible to admit such claims requests.

What is the unclaimed amount?

The unclaimed amount is money that is due to the Life Assured claimant in the form of a surrender or Freelook in cancellation but the payment has failed (reasons include incorrect bank details provided by the customer at the time of request, inactive bank account etc.). Such amounts are moved to an unclaimed account after 180 days from the date of payment failure.

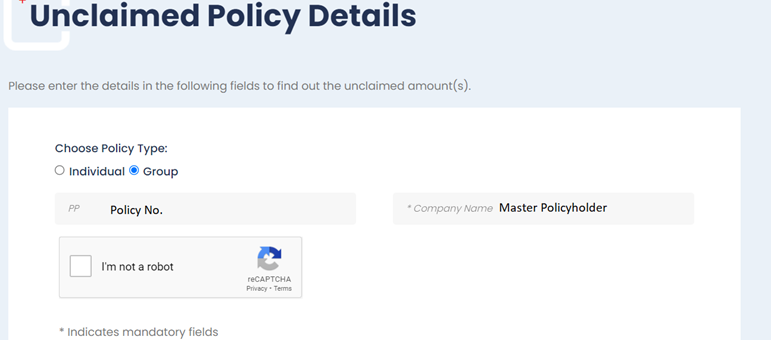

Where can I check the unclaimed amount to be received my request?

You can now visit https://www.hdfclife.com/customer-service/claims/unclaimed-policyholder-payment-dues-amount-disclosure to check the unclaimed amount for your request, if any. Please select ‘Group’ as the policy type(refer to the below screenshot) and then enter the ‘Master Policy no.’ and ‘Master Policyholder name’ (as per the first page of the copy of the Certificate of Insurance). Please refer to the template below -

After submitting the above details, you can search (Ctrl+F) for your unclaimed amount with the last 7 digits of Certificate No. (mentioned on the first page of COI).

How to redeem my amount which is still unclaimed?

To redeem your unclaimed amount, kindly share the following with [email protected] :

1. Personalized cheque/bank passbook copy of the claimant

2. Self-Certified PAN card copy

3. Address proof of claimant

4. Copy of COI

Kindly mention your Policy No. and Loan Account no * while writing to us (please refer to the attached format).

Subject: Unclaimed: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

TDS will be applicable as per existing Income Tax laws on any interest accrued.

*Please check the first page of the copy of the Certificate of Insurance for Policy No. and Loan account no.

4 PMJJBY - Group Term

Frequently asked questions on Pradhan Mantri Jivan Jyoti Yojana.

What are the documents required to acquire PMJJBY policy?

Below are the list of documents required to acquire PMJBY policy

- Application Form

- Member List

- PAN Card of Master Policy Holder

- Cheque Copy/Fund Details

- SOP

- Standing Instructions

What is the sum assured under PMJJBY policy?

INR 2,00,000.

What all documents are required at the time of renewal of the PMJJBY policy?

Documents are not required. Only funds and member data is required.

What if someone wants to discontinue the membership?

One can leave the membership within 15 days from the date of enrolment.

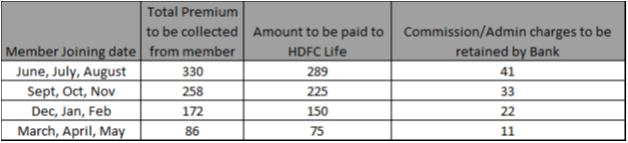

Can we take the policy any time during the year?

Yes, one can take the policy any time during the year. However, the policy will end on 31stMay of that financial year. The premium will be charged on a pro-rata basis as per below table:

What is the eligibility to get the policy under this scheme of government?

- Any Savings Bank Account holder aged between 18 and 50.

- Minimum age at entry - 18 years (as per last birth date) and maximum age at entry - 50 years (neared birth date) for new members.

- Maximum age – 55 Years (neared birth date) for existing members.

- The policy holder shall ascertain the eligibility of Scheme Member basis age

- Inaccurate information detected at claims stage will lead to repudiation of claims

Can Master Policy holder Surrender the policy?

Yes, within 15 days from the date of policy issued or renewed.

5 Group Health Shield

Which documents are required for new business of Non Employer Employee (NEE)?

The documents required are as follows:

- Proposal form

- Premium Rates Table signed & soft copy/ NML limits

- Standard Operating Process (SOP)

- Pan Card - Pan card copy of the Policyholder and authorized signatory

- Cheque copy or Fund transfer details

- Member data in uploader file format (Soft copy)

- Float amount needs to be collected as per SOP

- Certificate of Registration granted by RBI (For Regulated business) or Certificate of Incorporation (For Non Regulated business)

- Credit Life / Affinity quote template signed by Partner and Account management team

What details are required for a domestic fund transfer (within India)?

Details of Fund transfer are as below:

Bank Name |

HDFC Bank Ltd. |

Bank Address |

HDFC Bank Ltd. |

Bank A/C No. |

00602300010866 |

A/C Name |

HDFCSL CREDIT PROTECT |

IFSC Code |

HDFC0000060 |

Which products are covered under the Group Health Shield plan?

Group Health Shield (GHS) covers Group Health Credit (GHC) & Group Health Term (GHT).

What is the minimum policy term for GHS that can be opted for?

1 Year.

What is the maximum policy term for GHS that can be opted for?

5 Years.

What is the minimum entry age acceptable in GHS policy?

1 Year.

What is the Free Look in period for GHS policy?

15 Days.

What is the Grace Period for renewal of GHS policy?

30 Days.

Is Suicide Clause applicable in GHS?

No

Is there any Maturity Benefit in GHS?

No

What is the processing TAT for various processes?

Refer below grid for TAT details.

Processes |

TAT |

New Business |

T+7 |

Issuance |

T+3 |

Refund Payout |

T+3 |

Alteration |

T+1 |

* Only working Days need to consider for Above TAT |

|

6 Group Claims - Claimant section

Who can intimate a claim?

The Nominee can intimate a claim. If the Nominee is minor, the Appointee can intimate a claim on behalf of the minor Nominee. In case of unfortunate events of the contractual parties, the claim can be intimated by the legal heir with proof of legal title.

How to report a claim?

The claim form, fully filled and signed by the Beneficiary along with other mandatory documents (please refer to Q4.) should be submitted to the Master Policyholder (MPH) for their stamp and signature. MPH will then share the documents with HDFC Life along with the Member Information Form, Loan sanction letter & outstanding loan amount as of the date of the event.

Also, your claim can be lodged in any branch of HDFC Life or you can write to us at [email protected]. Please note that further requirements, if any will be raised with the MPH/Nominee.

Which claim form has to be submitted?

The claim form to be chosen depends on the policy issued to Life Assured. Please seek the assistance of MPH to choose the correct form:

What are the mandatory documents to intimate the claim?

Please refer to the Claim form for the mandatory documents to be submitted along with the claim. Ensure that the claim form is completely filled & signed by the Claimant and the MPH.

For your quick reference, click on the below link for the list of mandatory documents.

In case of multiple policies, what documents are to be submitted?

For Multiple Policies the Nominees will have to fill in separate Claim Intimation Form along with all requisite documents. Multiple copies of documents pertaining to affected person need not be submitted.

What are the mandatory fields in claim form to be filled by the claimant?

NMFI claim form - All Sections except Section VI have to be completely filled and signed by the Claimant before submitting the claim form to the MPH. Section VI to be filled up by the MPH.

MFI claim form - All Sections except Section V have to be completely filled and signed by the claimant before submitting the claim form to the MPH.Section V to be filled up by the MPH.

GTI claim form - All Sections except Section V – Declaration of Master Policyholder have to be completely filled and signed by the claimant before submitting the claim form to the MPH.Section V to be filled up by the MPH.

PMJJBY claim form - All Parts except Part 3 have to be completely filled and signed by the claimant before submitting the claim form to the MPH. Part 3 to be filled up by the bank

.

Please refer the pre-filled NMFI claim form for your reference. MFI/GTI/PMJJBY claims are to be similarly filled.

What is the time frame within which the claim has to be reported?

You should report a claim as soon as possible, to help us process it faster.

What is the benefit payable if the insured event occurring during the term of the policy?

Please refer the copy of Certificate of Issuance (COI) to understand the claim benefits payable as per the applicable T&C of your policy.

Please refer Appendix A of COI for Schedule of Benefits payable for your policy..

Please refer Appendix B of COI for Exclusions /Rider Benefits.

What is the Turn Around Time (TAT) for processing your claim?

TAT as per IRDAI guidelines |

Death/Rider Claims |

Claim Settlement/Repudiation/Rejection (Investigation not required) |

Within 30 days from the date of receipt of last requirement |

Claim Settlement/Repudiation/Rejection (Investigation is required) |

An investigation is to be completed not later than 90 days from the date of receipt of claim intimation and the claim decision is to be taken within 30 days thereafter. |

If we are unable to settle within the above TAT, your claim will be settled along with a penal interest at the rate of 2% above the bank rate* (prevalent at the beginning of the financial year) on the claim amount.

*Rate to be calculated from the date of receipt of the last requirement to the date of payment of the claim. TDS will be applicable as per the existing Income Tax rules.

In case of further claim-related queries/claim status, whom should you connect with?

You can now check the claim status on real time basis. Click on Track Claim status tab and enter your Group Policy details to view the status of your claim.

Further you can connect with the Master Policyholder for any queries regarding your claim.

Alternatively, you can also write to us at [email protected]. Your queries will be addressed within 5 working days. (Please refer to the below format while writing to us.)

Kindly ensure the below is mentioned in your mail:

Master Policy No. and Loan Account number*

Copy of Certificate of Insurance attached

Subject line as per below-attached format:

For Queries:

To: [email protected]

Subject: Query: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

For Complaints:

To: [email protected]

Subject: Complaint: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

*Please check the first page of the copy of the Certificate of Insurance for Master Policy No. and Loan account no.

What documents are to be submitted in the event of the death of the nominee?

In the event of the death of a life assured, the claim proceeds are to be given to the nominee. However, in the unfortunate event of the death of the nominee(as per the Member Information Form), Open Title documents are to be submitted along with the mandatory claim documents mentioned in Q4.

Open Title documents:

1) Advance Discharge Voucher

2) Application To Dispense With Legal Evidence Of Title

4) Nominee death certificate in 12/17 format

5) Legal Heir certificate / Succession Certification

What is the unclaimed amount?

The unclaimed amount is money that is due to the claimant in the form of a death claim/rider claim which is settled but the payment has failed (reasons include incorrect bank details provided by the claimant at the time of claim intimation, closed claimant account etc.). The Claim amount is moved to an unclaimed account after 180 days from the date of payment failure.

Where can you check the unclaimed amount to be received for your claim?

You can now visit https://www.hdfclife.com/customer-service/claims/unclaimed-policyholder-payment-dues-amount-disclosure to check the unclaimed amount for your claim. Please select ‘Group’ as the policy type(refer to the below screenshot) and then enter the ‘Master Policy no.’ and ‘Master Policyholder name’ (as per the first page of the copy of the Certificate of Insurance).

After submitting the above details, you can search (Ctrl+F) for your unclaimed amount with the last 7 digits of Certificate No. (mentioned on the first page of COI).

How to redeem your claim settlement amount which is still unclaimed?

To redeem your unclaimed settlement amount*, kindly share the following with [email protected]:

1. personalized cheque/bank passbook copy of the claimant

2. self-certified PAN card copy

3. Address proof of claimant

4. Copy of COI

Kindly mention your Policy No. and Loan Account no ** while writing to us (please refer to the attached format).

Subject: Unclaimed: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

**Please check the first page of the copy of the Certificate of Insurance for Policy No. and Loan account no.

*TDS will be applicable as per existing Income Tax laws on any interest accrued.

Would the claim be paid in foreign currency?

The claim would be paid in Indian Currency (INR) only

What is the list of illnesses covered under your Critical Illness rider benefit for your policy?

Please refer the Appendix B of the Certificate of Insurance to understand the list of illnesses covered as part of the Accelerated Critical Illness benefit of your HDFC Life policy (as per T&C).

On what grounds can your claim be rejected/repudiated/ made invalid?

Your claim can be rejected/repudiated/ invalid due to the following reasons:

Claim Rejected |

Claim Repudiated |

Claim Invalid |

|

|

|

*The above reasons are indicative and not exhaustive.

How do I represent a claim which is repudiated?

In case you wish to represent your claim to the Company, you may send a written request (duly signed by the claimant) to [email protected] within 30 days of receipt of the repudiation/rejection letter on the following address:

Claims Review Committee

HDFC Life Insurance Company Limited

11th Floor, Lodha Excelus, Apollo Mills Compound,

N.M. Joshi Road, Mahalaxmi,

Mumbai - 400 011

Maharashtra

Please mention your Master Policy no. and Loan Account no.* Please check the first page of the copy of the Certificate of Insurance for Policy No. and Loan account no. while writing to us. (please refer to the attached format).

Subject: CRC: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

If you are not satisfied with the response provided by the Claims Review Committee, where do you represent your claim?

If you are not satisfied with the response provided by the Claims Review Committee, you can also approach the Insurance Ombudsman in your region whose address is mentioned below. This address is available on our website https://www.hdfclife.com/

Alternatively, to locate any Ombudsman office, please click on https://www.cioins.co.in/Ombudsman

What is Section 45 of the Insurance Act 1938?

A policy of life insurance may be called into question at any time within three years from the date of issuance of the policy or the date of commencement of risk or the date of revival (if applicable) of the policy or the date of the rider to the policy, whichever is later, on the ground that any statement of or suppression of a fact material to the expectancy of the life of the insured was incorrectly made in the proposal or other document on the basis of which the policy was issued or revived or rider issued.

7 Group Claims – Master Policyholder (MPH) section

Who can intimate a claim?

The Nominee can intimate a claim. If the Nominee is minor, the Appointee can intimate a claim on behalf of the minor Nominee. In case of any unfortunate event of the contractual parties, the claim can be intimated by the legal heir with proof of legal title.

Where do you register a Fresh Claim?

You need to upload the documents in Life Next Portal provided by HDFC Life

Which claim form is to be submitted?

The claim form to be chosen depends on the policy issued.

What are the mandatory documents to intimate the claim?

Please refer to the Claim form for the list of mandatory documents to be uploaded along with the claim form. Ensure that the claim form is completely filled & signed by the Claimant before uploading it on Life Next.

For your quick reference, click on the below link for the list of mandatory documents.

- For Non-Employer Employee (NMFI) policy

- For Non-Employer Employee (MFI)

- For Employer-Employee (GTI - Group Term Insurance) policy

- For PMJJBY policy

Do you need to update the Claimant’s mobile no./email IDon Life Next?

Yes, the Claimant’s mobile no./email IDhas to be updated on Life Next by the MPH to ensure the claimant receives communication at all claim stages.

In case of multiple policies, what documents are to be submitted?

For Multiple Policies, the Nominees will have to fill in a separate Claim Intimation Form along with all requisite documents. Multiple copies of documents pertaining to an affected person need not be submitted.

What are the mandatory fields in a claim form to be filled by Master Policyholder (MPH)?

NMFI claim form - Section VI to be filled up by MPH.

MFI claim form - Section V to be filled up by MPH

GTI claim form - Section V Declaration of Master Policyholder: to be filled up by MPH

PMJJBY claim form - Part 3 to be filled up by the bank

Please note all other sections in the claim form are to be filled by claimant before uploading in Life Next.

Is the Member Enrollment form (MEF) / Member Authorization form (MAF) required?

Yes, MEF/MAF is required at the time of claim evaluation and has to be provided by the MPH. The same is provided at the time of policy issuance.

Will additional documents be requested once a claim is submitted?

Additional documents can be raised on a case-to-case basis. We will raise the request on LifeNext portal or the same would be communicated to you through our Sales team.

Do you need to dispatch hard copies of claim documents received from the Claimant?

Yes, the documents have to be couriered to the below address:

Akshay Pol/Govind Gurav

SeshaasaieForms Pvt. Ltd.

201, Mayuresh Chambers, Plot 60, Sector 11, CDB Belapur,

Navi-Mumbai

Maharashtra

Pin: 400614.

What is the benefit payable if the insured event occurs during the term of the policy?

Please refer to the copy of the Certificate of Issuance (COI) to understand the claim benefit payable as per the applicable T&C of your policy.

Please refer Appendix A of COI for the Schedule of Benefits payable for your policy.

Please refer Appendix B of COI for Exclusions.

What is the time frame within which the claim has to be intimated?

You should intimate a claim as soon as possible, to help us process it faster.

What is the Turn Around Time (TAT) for processing your claim?

TAT as per IRDAI guidelines |

Death/Rider Claims |

Claim Settlement/Repudiation/Rejection (Investigation not required) |

Within 30 days from the date of receipt of the last necessary document |

Claim Settlement/Repudiation/Rejection (Investigation is required) |

The investigation is to be completed not later than 90 days from the date of receipt of claim intimation and the claim decision to be taken within 30 days thereafter. |

If we are unable to settle within the above TAT, the claim will be settled along with a penal interest at the rate of 2% above the bank rate* (prevalent at the beginning of the financial year) on the claim amount.

*Rate to be calculated from the date of receipt of the last requirement to the date of payment of the claim. TDS will be applicable as per the existing Income Tax rules.

In case of further claim-related queries/claim status, whom should you connect with?

Claim status can now be tracked on real time basis. Click on Track Claim status tab and enter the Group Policy details to view the status of the claim.

For any queries, please write to us at [email protected]. Kindly ensure the below is mentioned in your mail:

Group policy No. and Loan Account number*

Copy of Certificate of Insurance attached

Subject line as per below-attached format:

For Queries:

To: [email protected]

Subject: Query: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

For Complaints:

To: [email protected]

Subject: Complaint: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

*Please check the first page of the copy of the Certificate of Insurance for Policy No. and Loan account no.

Alternatively, you can also check the claim status on the Life Next portal.

What documents are to be submitted in the event of the death of the Nominee?

In the event of the death of a Life Assured, the claim proceeds are to be given to the Nominee. However, in the unfortunate event of the death of the Nominee (as per Member Information Form), Open title documents are to be submitted to the Insurer. This includes the below set of documents:

Open Title documents :

2) Application for dispensing legal evidence

4) Nominee death certificate in 12/17 format

5) Legal Heir certificate / Succession Certification

What is the unclaimed amount?

An unclaimed amount is a money that is due to the claimant in the form of a death claim/rider claim but has not been claimed for more than 6 months since the settlement. Major reasons for this include the payment failure due to incorrect bank details provided by the Claimant at the time of claim intimation, closed claimant account etc.

Where can you check the unclaimed amount to be received for your claim?

You can now visit https://www.hdfclife.com/customer-service/claims/unclaimed-policyholder-payment-dues-amount-disclosure to check the unclaimed amount for your claim. Please select ‘Group’ as the policy type (refer below screenshot ) and then enter the ‘Policy no.’ and ‘Master Policyholder name’ (as per the first page of the copy of the Certificate of Insurance).

After submitting the above details, you can search (Ctrl+F) for your unclaimed amount with the last 7 digits of Certificate No. (mentioned on the first page of COI).

What documents are to be provided for receiving an unclaimed settlement amount?

If the amount* is payable to the Nominee, kindly share the following to [email protected]:

Personalized cheque/bank passbook copy of the claimant

- Self-certified PAN card copy

- Address proof of claimant

- Copy of COI

Please mention your Group policy no. and Loan Account no.** while writing to us. (please refer to the attached format).

Subject: Unclaimed: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

**Please check the first page of the copy of the Certificate of Insurance for Group policy No. and Loan account no.

*TDS will be applicable as per existing Income Tax laws on any interest accrued.

If the amount is payable to the MPH, please ensure the submission of MPH account details to us at [email protected]. Please note that the base amount of the claim would be settled in favor of the MPH & the interest would be settled in favor of the claimant’s account details.

What is the list of illnesses covered under your Critical Illness rider benefit for your policy?

Please refer the Appendix B of the Certificate of Insurance to understand the list of illnesses covered as part of the Accelerated Critical Illness benefit of your HDFC Life policy (as per T&C).

On what grounds can your claim be rejected/repudiated/ made invalid?

Yes, the claim can be rejected/repudiated/invalid due to the following reasons*.

Claim Rejected |

Claim Repudiated |

Claim Invalid |

|

|

|

*The above reasons are indicative and not exhaustive.

How does a claimant represent a claim which is repudiated?

In case a claimant wishes to represent his/her claim to the Company, he/she may send a written request (duly signed by the claimant) to [email protected] within 30 days of receipt of the repudiation/rejection letter at the following address:

Claims Review Committee

HDFC Life Insurance Company Limited

11th Floor, Lodha Excelus, Apollo Mills Compound,

N.M. Joshi Road, Mahalaxmi,

Mumbai - 400 011

Maharashtra

Please mention your Group policy no. and Loan Account no.* while writing to us. (please refer to the attached format).

Subject: CRC: Group Policy No: <type your Group Policy no.>, LAN: <type your loan account no.>

If a claimant is not satisfied with the response provided by the Claims Review Committee, where does represent the claim?

If a claimant is not satisfied with the response provided by the Claims Review Committee, he/she can also approach the Insurance Ombudsman in your region whose address is mentioned below. This address is available on our website https://www.hdfclife.com/

Alternatively, to locate any Ombudsman office, please click on https://www.cioins.co.in/Ombudsman

What is Section 45 of the Insurance Act 1938?

A policy of life insurance may be called into question at any time within three years from the date of issuance of the policy or the date of commencement of risk or the date of revival (if applicable) of the policy or the date of the rider to the policy, whichever is later, on the ground that any statement of or suppression of a fact material to the expectancy of the life of the insured was incorrectly made in the proposal or other document on the basis of which the policy was issued or revived or rider issued.

You can let us know of your concerns through any of our touch points mentioned below.

- Option 1: You can visit the nearest HDFC Life branch. To know more about branch address & timing's click here branch locator.

NOTE: Branches are closed on Sundays, national holidays and region-specific public holidays.

- Option 2: Call us between 10 AM – 6 PM (Mon - Fri ) on the HDFC Life Group Claims No. 022 6751 6250 (Local Charges Apply). DO NOT prefix any country code e.g. +91 or 00.

- Option 3: Write to us from your email ID at [email protected]. If your concerns are not satisfactorily resolved, you are requested to submit the same online by filling out the form below.

- Option 4: Escalation matrix :

Original: Group Claim

Email Id: [email protected]

022 6751 6250

Please fill the form below to share your concern.

- Fields marked with "*" are mandatory to be filled.

- Name must be identical to that mentioned in your Certificate of Insurance (COI)

State Your Concern

Section I: Master Policy Holder Details

INT/GS/03/23/1404