- Webpages

- Documents

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

-

![login]() Customers

Customers

-

![login]() Employees

Employees

-

![login]() Partner

Partner

- Consultants

- Partner Portal-FC

For NRI Customers

(To Buy a Policy)

-

![Contact Image]()

Call (All Days, Local charges apply)

-

![Contact Image]()

Email ID

-

![Contact Image]()

Whatsapp

(If you're our existing customer)

-

![Contact Image]()

Call (Mon-Sat, 10am-9pm IST, Local Charges Apply)

-

![Contact Image]()

Email ID

For Online Policy Purchase

(New and Ongoing Applications)

-

![Contact Image]()

Call (All Days & Toll free)

-

![Contact Image]()

Schedule a call

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Give missed call to buy a policy

-

![Contact Image]()

Email

Branch Locator

-

![Contact Image]()

Locate a branch

For Existing Customers

(Issued Policy)

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Call (Mon to Sat, from 10 am to 7 pm, Call charges apply)

-

![Contact Image]()

Email

Fund Performance Check

-

![Contact Image]()

Call (Missed Call)

-

Life coverage

-

Tax Benefits5

-

Guaranteed1 Income

What is a Pension Calculator?

A pension calculator is an easy-to-access online tool that allows you to estimate the pension income you can receive after retirement. To calculate your pension income, the tool considers parameters such as your salary, age, current savings, years of service and future contributions. Entering all these details in the calculator enables you to plan savings over time, stay on the right track and achieve your desired financial goals once you retire.

Overall, this pension calculator is a user-friendly financial tool that lets you save time and effort and provides valuable insights into your retirement needs. Additionally, you can adjust the parameters and try out different combinations to choose the best retirement plan. While you are planning to choose a retirement plan in India, consider the plan with a guaranteed sum that will meet your financial needs and objectives.

Since retirement planning is a long-term financial goal, start early to experience the benefits of compounding. Moreover, efficient use of a pension calculator also lets you plan your retirement income effectively and provides you with a clear picture of the pension amount you should expect post-retirement.

How Does a Pension Calculator Work?

A pension calculator provides a quick estimate of retirement income considering several parameters and mathematical models. The primary aim of this calculator is to experience the benefits of future pensions and allow individuals to lead a stressful life post-retirement.

For accurate use of this calculator, you need to provide all relevant details such as your age, income, gender, smoking habits, gender and other factors including the tenure of payment of premiums, the amount you wish to invest, mode of premium payment and others. Once you enter all this information, the calculator yields output relating to the premium amount, term of premium payment and the annuity amount.

Taking into consideration your age and the amount you wish to invest in your chosen retirement plan, the calculator multiplies this amount with a compounding rate to provide an estimate. This is the retirement corpus you can save over a set period and enjoy your post-retirement life.

Here is the retirement income formula used by pension calculators:

FV = PV (1+r) ^n

Where, FV denotes the future value, PV is the present value, r is the expected rate of inflation, and n is the desired time of retirement.

For example, if you plan to receive Rs. 20, 00,000 annually after retiring, calculate the retirement income with an estimated 8% return, an inflation rate of 6% and a period of retirement of 20 years. Entering these values in the above formula provides you with the retirement income you aim to receive after retirement.

Secure Your Retirement with Our Pension Plans

Planning Your Pension

Follow the given steps to make a proper retirement plan:

1. Understanding Pension Needs

Proper planning and a long investment horizon are essential to get a consistent pension income. By opting for the right pension plan, you can inculcate the habit of investing regularly and build a lump sum retirement corpus. A pension plan is a long-term investment plan that lets you pay in small amounts and regularly.

Make sure to start saving for retirement at an early stage of your career to save a huge amount during your retirement time.

2. Key Planning Components

Proactive planning for your retirement income is essential. Let’s go through the key planning components in detail below:

a) Monthly Contribution Assessment

Your capability of contributing to your pension income on a monthly basis determines your retirement savings. Begin by carefully assessing your monthly income, savings, and expenditures. Following the rule of thumb, allocating at least 10-15% of your monthly income towards retirement savings is mandatory. Alongside this, make sure to review the monthly contribution and raise the amount regularly to build a strong retirement corpus over time.

b) Risk Profile Determination

Understand your risk appetite to align your investment goals with post-retirement income. By starting to invest at an early age, you can avail better investment opportunities and benefit from the power of compounding. Whereas, if you start investing when nearing retirement, you can only choose low-risk investment options. By assessing your risk profile, you can reduce stress and reach your desired goals.

c) Investment Horizon Planning

Investment horizon plays an important role towards retirement planning. Opting for a longer horizon allows you to accumulate a bigger retirement corpus, leveraging the power of compounding. Moreover, you can invest in riskier assets, as you have enough time to recover from market corrections.

As you approach retirement, you need to gradually shift your allocations towards conservative assets to preserve your wealth.

d) Tax Efficiency Consideration

Considering tax-advantaged investments like the Employee Provident Fund (EPF) can result in enhancing your savings. Consistent investment in this account often results in reduced taxable income and you can find your savings to grow as tax exemption. Thus, gaining a proper understanding of these implications of taxes is crucial for withdrawing net amount post-retirement and maximising your income.

3. Age-Based Pension Milestones

The rule for retirement planning is that the earlier you start investing, the more you can save. However, with age comes changes in priorities. From starting to save in your early 20s to making adjustments in investment strategies in your 50s, each stage of life requires a comprehensive approach.

Here is a detailed overview of appropriate retirement strategies at different stages of your life:

a) Early Career (25-35)

This is the earliest phase of a career with minimum responsibilities. Individuals are encouraged to start planning for their future. Though many people consider this phase too early for retirement planning, planning early at a young age is recommended for the maximum benefits from the market.

With early retirement planning and investment, you can benefit from the power of compounding. Secondly, you can choose from a wide array of investment options. Even if you make losses, there will be plenty of options and time to compensate for it.

b) Mid-Career (35-45)

In this phase of life, you have added responsibilities. Most people in this age group are married and have children. Thus, the financial expenditure is also higher. Moreover, many people even choose to purchase their dream home or car or invest in other assets.

All these can interfere with your retirement goals. To stay on the right track, make sure to prepare a budget covering all monthly expenses that include repayment of loans, school fees, electricity, payment of premiums, retirement contributions, etc.

c) Late Career (45-55)

This phase of life is comparatively stable in comparison with stages before. You should expect to receive a steady salary in this phase. Your retirement savings during this time are also expected to reach a decent figure.

However, with an increase in your salary and income, the standard of living also grows. This makes it necessary to save a portion of your income. Stay focused towards your financial goal at this stage and make sure to grow your savings fighting against inflation.

Most importantly, if you have not started to save, this phase of life will be ideal to start as you have just 20 more years to get prepared for your financial future.

d) Pre-retirement (55+)

This stage is when you are nearing your retirement period. Most people prefer to retire during their 60s, thus, 50s is a crucial time for understanding your investment and savings strategies.

It is advisable to choose a less risky investment plan as any unexpected loss will be hard to deal with. Other than this, you can raise your retirement contribution as you will have comparatively fewer responsibilities at this age. Your children are grown up, and they have become financially independent. Thus, now you will have more money to invest or save to attain your financial goals.

Understanding Pension Types and Benefits

Pension plans provide financial support to individuals during years of retirement and ensure stability. The benefits and returns vary across different types of plans. Gaining a proper understanding of the different types of pension plans ensures securing your financial future and achieving your well-being.

Let’s look into the different types of pension plans in detail:

1. Government Pension Schemes

Government pension schemes are preferable because of their distinguishing feature of offering financial security to individuals post-retirement. These schemes are usually funded through contributions from employers, workers and tax collection. Moreover, government schemes provide a steady source of income and are adjusted for inflation. By opting for this plan, individuals can get a predefined pension income after retirement.

2. Employee Pension Plans

The Employee Provident Fund (EPF) was introduced by the EPFO (Employee Provident Fund Organization) during the period 1995. This plan aims towards providing financial security and stability to employees in terms of income post-retirement. The EPFO ensures that all employees receive the desired pension amount after crossing the age of 58 years.

12 percent of the basic salary of an employee along with dearness allowance adds as a contribution towards the Employee Pension Plan each year. It’s a mandatory pension scheme for private sector employees that provide various tax benefits.

3. Private Pension Options

Private pension options are different plans of retirement offered by employers or any other financial institution. With this option, individuals can continue saving and investing to secure their lives post-retirement. Alongside this, a private pension offers flexibility in selecting different strategies of investment considering your risk appetite.

4. NPS and Other Instruments

Any individual between the ages of 18 and 70 years is eligible to opt for the National Pension System (NPS). With this retirement plan, you can avail tax benefits of up to Rs. 2 lakh in any particular financial period. If you have a moderate to high-risk appetite, this plan will be an ideal option.

Investors in this plan can choose to invest in corporate bonds, equities and any other alternative investment funds. Once you reach the age of 60 years and above, your NPS account matures, and you can further utilise this amount to purchase annuities and receive a fixed pension after retirement.

5. Comparison of Benefits

Let’s look into the different factors you should consider when comparing pension plans:

a) Returns Potential

Government pensions usually pay stable, but modest returns, as they are financed through taxes or fixed contributions. Private pensions, such as life insurance plans and ULIPs, can offer higher returns since they invest in stocks, bonds, or mutual funds. However, these returns are market-dependent. To better understand the potential returns and determine the optimal life insurance coverage for your retirement, you can use a life insurance calculator to help assess your needs based on your financial goals.

b) Risk Factors

Choose pension plans with low risk and offering guaranteed comprehensive payout without being affected by market ups and downs. Whereas, private pension plans have high risk associated because of their dependability on investment choices and market fluctuations.

c) Tax Advantages

There are many pension plans offering tax benefits. Government schemes are exempted from taxes, thereby lowering the taxable income. However, pension income withdrawal from private plans might charge taxes. Thus, it's essential to understand its benefits.

d) Withdrawal Rules

There are many government pension plans with a fixed age for withdrawals. Whereas, private pensions provide flexibility and allow you to withdraw early in certain cases, though heavy penalties might apply. Thus, understanding the withdrawal rules is a must when you need emergency funds.

Factors Affecting Pension Calculations

Here are the factors to consider that affect pension calculations:

1.Economic Factors

There are some economic factors that influence pension calculations significantly. Here is a detailed explanation of the two most important factors – inflation and rates of interest.

a) Inflation Impact

Inflation denotes the rise in the general price of products and services, decreasing people’s purchasing power. Over time, the same sum of money lets people purchase fewer goods and services due to inflation. If your pension savings are not adjusted for inflation, it might be challenging for you to maintain a desired standard of living post-retirement.

Thus, a high rate of inflation raises your post-retirement expenses required to maintain a good standard of living.

b) Interest Rate Fluctuations

Fluctuations in market interest rates create an impact on the growth of pension savings. When interest rates in the market fall, the investment returns on fixed income reduce, requiring investors to save higher amounts to meet their desired financial goals. Thus, close monitoring of interest rates is crucial to minimise risks and calculate pension amounts efficiently.

2. Personal Factors

There are several factors that influence pension calculations alongside ensuring financial stability post-retirement. These factors however vary from one individual to another and are tailored to meet the needs and preferences of individuals.

a) Life Expectancy

Life expectancy plays a crucial role in retirement planning and for planning allocation of assets. Individuals with longer life expectancies need to have more savings. Actual estimations of life expectancy help in understanding how long funds can last considering the contribution amount and chosen investment strategies.

For instance, an individual with an expectation of living up to 90 years must have a comprehensive pension plan in comparison with a shorter life expectancy individual. Your current lifestyle, medical history and habits determine your life expectancy.

b) Lifestyle Requirements

Lifestyle requirement is an important factor towards determining pension needs. Individuals leading a moderate standard of living might need less funds than those maintaining a higher standard of living. Thus, the needs of pension income depend on an individual's lifestyle preferences. The income should be adequate enough to sustain the financial goals without worrying about the future.

c) Healthcare Needs

Healthcare is an unpredictable factor towards assessing pension income. With ageing, medical expenses increase, ranging from routine checkups to long-term medical treatments. Assessing these healthcare costs is essential to assess financial needs. On the other hand, individuals with a family history of illness must keep extra funds aside for healthcare.

3. Market Factors

Considering market factors is crucial for retirement planning with pension calculators. Both the investment returns and performance of investments have an impact on the retirement savings you can get. Here is a detailed overview of these factors:

a) Investment Returns

When deciding where to invest your funds, the past returns and future expected cashflows of an asset should be considered. Investing in stocks, mutual funds, bonds and other high-yield assets is advisable for higher returns. However, fluctuations in the market can provide unpredictable returns. Thus, you should consider your risk appetite and choose the right investment strategy to avail high returns.

b) Fund Performance

The overall performance of a pension fund also plays a crucial role towards determining its future value. If your chosen funds perform poorly, it can negatively impact your savings. Thus, you must review your investment plans regularly and shift to other investment plans if necessary.

How to Use the HDFC Life Pension Calculator?

The HDFC Life Pension calculator is a simple and hassle-free online financial tool that lets you estimate the amount you can get once you retire. Here is a detailed step-by-step guide to follow after visiting the HDFC Life Pension calculator page:

Step 1: Enter Your Date of Birth (DOB)

Fill in your date of birth (DD/MM/YYYY) to determine your age and the time left until retirement.

Step 2: Input Your Current Monthly Expenses

Enter your monthly expenses in ₹ to assess your financial needs post-retirement. This helps estimate the required pension amount.

Step 3: Specify the Expected Rate of Return (%)

Enter the rate of return you expect to get on the amount you are saving and investing to project the future value of your retirement fund.

Step 4: Enter Your Current Monthly Investments (₹)

Provide details of your monthly investments across various financial instruments like fixed deposits, mutual funds, stocks, or other retirement savings plans.

Step 5: Enter Your Full Name

Fill in your full name similarly to your official ID proofs like Aadhar card or PAN card

Step 6: Provide Your Mobile Number

Enter your mobile phone number in the provided field.

Step 7: Check Returns

Once you enter the details, click on “Check Returns” and get your estimated pension amount and accumulated corpus based on your inputs. You’ll get insights on how much more investments are required to reach your goals for retirement.

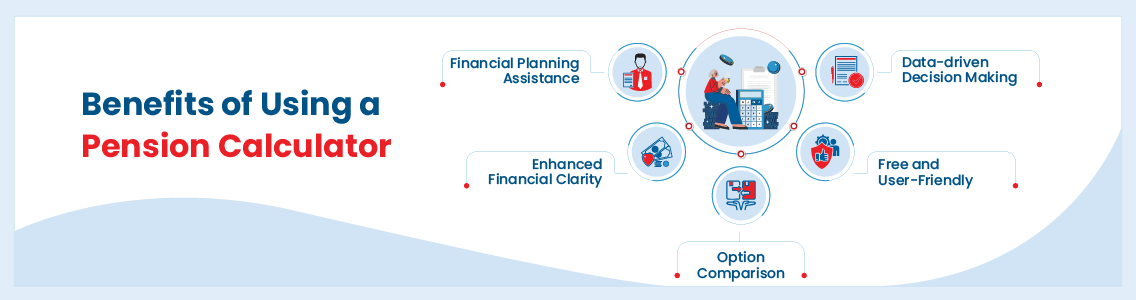

Benefits of Using a Pension Calculator

The notable benefits of using a pension calculator are explained as follows:

1. Financial Planning Assistance

With the use of a retirement planning calculator, determining the required amount for securing your retirement life is easier. This will help to allocate the necessary funds to meet desired financial needs, medical emergencies, etc., to lead a life without sacrificing your desired standards of living.

2. Enhanced Financial Clarity

The free pension calculator provides you with several options for determining the annuity amount. You can calculate the amount you need to fulfil your retirement goals and make an informed decision. If you have existing retirement plans, use the calculator to get clarity on the retirement corpus. By entering the relevant details, you can derive the monthly pension amount which you can receive post-retirement days.

3. Option Comparison

With different results derived from the retirement calculator, you can make a thorough comparison of the returns from different retirement funds, considering factors such as mode of premium payment, annuity option, and payment term. This way, you can choose the right retirement plan in India that aligns with your financial objectives.

4. Free and User-Friendly

The retirement and pension calculator is a free and easy-to-use friendly online tool. There is no need for technical expertise, and it is accessible from anywhere and anytime. All you need to do is provide detailed information. The pension calculator thereby displays the pension amount you ought to receive post-retirement.

5. Data-driven Decision Making

Efficient use of the online pension calculator enables individuals to reach an informed decision regarding their retirement plans. With this, individuals can also assess whether their investment strategies align with desired retirement goals. Moreover, with the pension calculator, complex calculations become simpler, allowing people to easily plan their investment strategies.

Creating Your Pension Plan

Planning your pension future is a crucial step to lead a secure and comfortable life. Let’s explore each of the factors in detail below:

1. Goal Setting Process

Start creating your pension plan once you identify your retirement goals. Be particular about the lifestyle you want to lead, your monthly expenditure and other goals such as healthcare expenses or travelling. Make a rough estimation of the amount you will need per year to meet your financial goals, considering inflation and rates of interest. This will set you on a clear path to achieve your desired goals.

2. Timeline Creation

Create a timeline for your pension plan. Calculate the number of years remaining until you retire and then break that into different phases of retirement years. Setting a clear timeline as per your age will help you stay focused and achieve your financial goals with ease.

3. Investment Strategy Development

Choose the right investment option for growing your retirement savings. Invest in the right strategy considering your risk appetite and scheduled retirement timeline. Ensure that you diversify your portfolio with options such as mutual funds, bonds, stocks, and retirement accounts. Starting to invest early provides you with various opportunities for investment with safer options.

4. Regular Review Schedule

Plan a specific schedule for reviewing your pension plan regularly, at least once a year. Need for money during an emergency might affect your financial plan. Thus, through regular reviews, you can ensure to keep your savings on track.

5. Adjustment Mechanisms

It’s important to adjust while creating a pension plan. If you face any financial shortage or a sudden increase in expenses, make changes in your contributions or revise your investment strategy. Adapting yourself as per your needs enables you to manage unforeseen challenges while maintaining your pension goals.

Conclusion

Planning for retirement can be a very overwhelming task, but a pension calculator simplifies the task. It provides insights into how much to save and where to invest for your desired lifestyle. Updating the calculator regularly with changes in your income or goals ensures you stay on track.

A well-planned retirement means financial freedom and peace of mind, allowing you to focus on what truly matters. Start using a pension calculator to take control of your finances and work towards achieving your perfect retirement from today.

FAQ's on Pension Calculator

1 How is pension calculated?

Pension is calculated by estimating the regular expenses you'll have post-retirement. An online pension calculator considers your age, expected retirement age, current income, and savings. This helps it estimate the total savings you will have at retirement and whether it is sufficient for your golden years. Using this information, the online pension calculator determines your expected monthly expenses after retirement.

2 What is the formula to calculate pension?

Plan your retirement income using the formula: FV = PV (1+r)^n, where FV is the Future Value, PV is the Present Value, r is the expected inflation (say 6%), and n is the time to retirement (say 25 years). For instance, if you need Rs 18,00,000 annually after retiring, calculate the corpus using an (estimated) 8% rate of return, a 6% inflation rate, and a retirement period of 20 years (assuming longevity of 20 years post retirement). The formula helps estimate the amount needed and the corpus required to generate the income for a secure retirement.

3 How much pension will I get for 10 years?

Using the retirement planning formula (FV = PV (1+r)^n), let's break it down. Assuming you're 35 with a Rs 50,000 salary, aiming to retire at 60, you have 25 years till retirement. If your desired annual post-retirement income is Rs 18,00,000, with an 8% return rate and 6% inflation, your pension calculation reveals the corpus needed for 10 years of post-retirement bliss.

Utilizing the formula provides insights into securing the ideal pension amount for the next decade, aligning with your financial goals and aspirations. For 10 years, you will get Rs 18,00,000 annually.

4 What will be my pension when I retire in India?

You are entitled to a fixed pension if you are a government employee. People working in private organisations and making PF contributions are eligible for pension under the Employees' Pension Scheme (EPS) on fulfilment of some terms and conditions.

In all other cases, you need to provide for your own pension after retirement. This can be done by investing in a pension plan while still working. The amount of pension you get after retirement will depend upon the amount you invest in the pension plan regularly, among other factors.

ALL CALCULATORS

-

Retirement Calculator

-

Income Tax Calculator

-

Pension Calculator

-

ULIP Calculator

-

Human Life Value Calculator

-

Cost Of Delay Calculator

-

Compound Interest Calculator

-

BMI Calculator

-

Investment Calculator

-

Child Education Planner

-

Marriage Expense Calculator

-

Term Insurance Calculator

-

SIP calculator

-

PPF Calculator

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance plans - protection, pension, savings, investment, annuity and health.

Popular Searches

- term insurance

- Best Retirement Plan

- Best Investment Plan

- 1 crore investment plan

- ULIP

- Best Savings Plan

- Compound Interest Calculator

- ULIP Calculator

- Income Tax Calculator

- Investment for beginners

- 5 year Investment Plan

- 10 year Investment Plan

- 20 year Investment Plan

- Child Insurance Plan

- ULIP vs. SIP

- Insurance vs. Investment

- Retirement Calculator

- nps vs ppf

- safest investment options

- one time investment plans

- types of investments

- health insurance plans

- Pension Calculator

- Long Term Investment Plan

- Short Term Investment Plan

- life Insurance policy

- life Insurance

- critical illness insurance

- Whole Life Insurance

- benefits of term insurance

- types of life insurance

- types of term insurance

- Benefits of Life Insurance

- Endowment Policy

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- best saving schemes

- Retirement Planning

- Annuity Calculator

1. The word “Guaranteed” and “Guarantee” mean that annuity payout is fixed once the policy has been purchased.

5. As per Income Tax Act, 1961. Tax benefits are subject to changes in tax laws.

18. Save 46,800 on taxes if the insurance premium amount is Rs.1.5 lakh per annum and you are a Regular Individual, Fall under 30% income tax slab having taxable income less than Rs. 50 lakh and Opt for Old tax regime.

This interactive does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. HDFC Life Insurance Company Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information reported by the interactive.

The information being provided through this interactive is provided for your assistance/ information only and is not intended to be and must not alone be taken as the basis for an investment decision (“Information”). The recipient/ user assume the entire risk of any use made of this Information. Each recipient /user of this interactive should make such investigation as it deems necessary to arrive at an independent decision while making an investment and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors. HDFC Life Insurance Company Limited and its affiliates, group companies, sales staff, financial consultants, officers, directors, and employees may have potential conflict of interest with respect to any recommendation, related information or opinions.

This Information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This Information is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject HDFC Life Insurance Company Limited and its affiliates/ group companies to any registration or licensing requirements within such jurisdiction. The distribution of this Information in certain jurisdictions may be restricted by law, and persons in whose possession this Information comes, should inform themselves about and observe, any such restrictions. The Information given in this interactive is as of the date of this report and there can be no assurance that future results or events will be consistent with this Information. This Information is subject to change without any prior notice. HDFC Life Insurance Company Limited reserves the right to make modifications and alterations to this statement as may be required from time to time. However, HDFC Life Insurance Company Limited is under no obligation to update or keep the Information current.

Neither HDFC Life Insurance Company Limited nor any of its affiliates, group companies, directors, employees, sales staff, financial consultants or representatives shall be liable for any damages whether direct, indirect, special or consequential including health, physical well being, lost revenue or lost profits that may arise from or in connection with the use of the Information. Past performance is not necessarily a guide to future performance.

ARN - ED/12/24/19207