- Webpages

- Documents

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

- HDFC Life ClassicAssure PlusInvestment

For NRI Customers

(To Buy a Policy)

-

![Contact Image]()

Call (All Days, Local charges apply)

-

![Contact Image]()

Email ID

-

![Contact Image]()

Whatsapp

(If you're our existing customer)

-

![Contact Image]()

Call (Mon-Sat, 10am-9pm IST, Local Charges Apply)

-

![Contact Image]()

Email ID

For Online Policy Purchase

(New and Ongoing Applications)

-

![Contact Image]()

Call (All Days & Toll free)

-

![Contact Image]()

Schedule a call

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Give missed call to buy a policy

-

![Contact Image]()

Email

Branch Locator

-

![Contact Image]()

Locate a branch

For Existing Customers

(Issued Policy)

-

![Contact Image]()

Whatsapp

-

![Contact Image]()

Call (Mon to Sat, from 10 am to 7 pm, Call charges apply)

-

![Contact Image]()

Email

Fund Performance Check

-

![Contact Image]()

Call (Missed Call)

- What Is a Life Insurance Policy?

- Why is it important to buy a Life Insurance Policy?

- Who can purchase a Life Insurance Policy?

- Types of Life Insurance Plan

- Differences Between Types of Life Insurance

- How Does A Term Insurance Policy Work?

- Life Insurance Coverage Amount Explained

- Benefits of Life Insurance Plans

- Important Terms About Life Insurance Plans in India

- How To Choose A Life Insurance Policy?

- Factors to Evaluate Before Deciding on Life Insurance Protection

- Dos And Don'ts When Dealing With Life Insurance Policies

- How to Select the Right Life Insurance Plan for Yourself and Your Family?

- How much Life Insurance cover does one need?

- Life Insurance Plans offered by HDFC Life

- What Is Human Life Value, And Why Should You Consider It Before Deciding On Your Life Cover?

- Should One Buy More Than One Life Insurance Policy?

- Riders in Life Insurance

- Steps to Buy Life Insurance Policy Online

- Documents Required to Buy a Life Insurance Plan in India

- How to Save Tax with Life Insurance Policy?

- How to File a Life Insurance Claim?

- How to Avoid Life Insurance Claim Rejection?

- Why Should Women Consider Investing In A Life Insurance Policy?

- Crucial Situations When You Should Consider Reviewing Your Policy

- FAQs on Life Insurance Policy

- Here's all you should know about life insurance

- Popular Searches

- Disclaimer

Life Insurance Plans

Life insurance plans help take care of your family’s financial needs if something unexpected happens to you. ...Read More

Protect Your Future with HDFC Life: Explore Our Life Insurance Plans!

ROP

Return of Premium^

Same Day

Claim Processing#

99.50%

Claim Settlement Ratio##

66 Million

Lives Insured@

₹3 trillion

Assets under

management@

630 Billion

Total Premiums@

TERM INSURANCE PLANS BUYING GUIDE

TERM INSURANCE PLANS BUYING GUIDE

Francis Rodrigues

Francis Rodrigues

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

Vishal Subharwal

Vishal Subharwal

Vishal Subharwal heads the Strategy, Marketing, E-Commerce, Digital Business & Sustainability initiatives at HDFC Life. He is responsible for crafting and ensuring successful implementation of the overall organisation strategy.

What Is a Life Insurance Policy?

Life insurance policy is like a safety net for your loved ones in the event of an unforeseen incident. It's a deal between you and an insurance company: you pay a small amount regularly, called a premium, and in return, they promise to give a sum of money to your family if you pass away during a certain time frame. Some policies also offer add-ons like coverage for serious illnesses or accidents. This extra protection can provide even more peace of mind for you and your family. In simple terms, life insurance plans ensure that your family will be financially secure even if you're no longer around to take care of them. It's an essential step in planning for the future and protecting the ones you love. For those living abroad, Life Insurance for NRI provides essential financial protection for families and dependents in India, ensuring their security even when the policyholder resides abroad.

Why is it Important to Buy a Life Insurance Policy?

Life insurance policy is more than just financial security; it's a crucial part of smart financial planning. Here’s why having a life insurance policy is so important:

Financial Security for Loved Ones

Life insurance plan offers vital financial stability for your family if you pass away. It provides a lump sum (death benefit) to cover expenses like mortgage, education costs, and daily living. This ensures your loved ones can maintain their lifestyle and focus on healing emotionally without financial worries during a challenging time.

Debt Repayment

The proceeds from your life insurance policy might be used to settle your outstanding loans and credit card payments. If the financial burden is lifted, the surviving family members may concentrate on creating a life unburdened by debt.

Income Replacement

When breadwinners or primary earners pass away, life insurance is a crucial tool for restoring family income. The death benefit of a life insurance policy considerably replaces income loss.

Funeral and End-of-Life Expenses

Expenses related to funerals and end-of-life care may place a significant financial strain on families during a difficult emotional period. Earnings from a life insurance plan may pay for expenses like a funeral and medical costs, letting loved ones focus on grieving and healing rather than worrying about money.

Estate Planning and Inheritance

Estate preparation is only complete with a life insurance policy, which may provide a steady cash stream to cover expenses like settlement costs and estate taxes. It helps with the smooth transfer of assets to beneficiaries, ensuring the right people receive their inheritance without any problems.

Future financial planning

Life insurance plans as an investment plan provides you the opportunity to grow your investments either with guaranteed returns or market linked returns depending on your risk appetite and financial goals.

Business Continuity

Life insurance policy is a wise investment for business owners who care about their partners' and stakeholders' well-being and the continuity of their activities. It could be useful for various reasons, including a buy-sell agreement, paying off corporate debt, or providing financial aid during a transition. All of these contribute to preserving the firm's history and value.

Peace of Mind

In the event of the policyholder's untimely death, the confidence that their loved ones would be financially supported is the most important advantage of life insurance policy. As a tangible expression of love and responsibility, it provides stability and solace among life's uncertainties.

Affordable Premiums

Thanks to a selection of coverage options and flexible payment plans, people may tailor their life insurance policy to match their needs and budgets.

Tax Benefits*

Owning a life insurance policy has many tax advantages. Premiums paid for a life insurance are applicable for tax savings with deductions under 80C, premiums paid for add-on riders are applicable for tax savings with section 80d, maturity benefits from a life insurance are applicable for tax savings under section 10(10D) as per applicable tax rules.

Saving for retirement

Solving for your retirement needs is crucial as you might not have a regular source of income post your retirement. Pension plans can provide you with a sustained regular income that can help you live a stress-free retirement.

Risk Management

Life insurance plan is crucial for risk management because it safeguards financial stability in the case of unforeseen circumstances. With this safety net, family members can better ride out life's storms.

Coverage Options

In life insurance policies, you may choose from a broad range of coverage options to suit your needs and preferences. Different types of life insurance provide various levels of protection. Term insurance gives short coverage, permanent insurance covers a lifetime, and investment-linked plans offer growth potential.

Who can purchase a Life Insurance Policy?

Life insurance is a financial tool providing significant security and peace of mind for both you and your loved ones. Insurance offers financial protection to your family in the event of your passing and helps them maintain their standard of living. If you are 20 and above, you must consider buying life insurance.

A life insurance policy can be bought by anyone who meets the following criteria:

Age Group

Citizenship

Other Aspects

Age Group |

Importance of Buying Life Insurance in a Specific Age |

20 - 30 years |

In this age group, individuals can get comprehensive insurance at a reasonable price. It can help with debt repayment (including school debts) and other costs, securing future financial goals including saving for a house, retirement, and more. |

30 - 40 years |

Depending upon the life insurance policy they choose, individuals in this age bracket can gain a reliable monthly income. They also get financial stability for the whole family, plan for children's higher education, marriage expenses, and more. |

40 - 50 years |

For this age group, life insurance plans are an opportunity to save for future needs like retirement and education for kids. |

50 and Above |

People who are 50 and above can invest in life insurance for financial security for themselves and family, gain tax benefits, and enhance savings. Among other benefits, it helps easily pay off large amounts owed to family members. |

Only applicants who are nationals or permanent residents of the issuing country can apply. However, international insurers sometimes provide unique coverage options for non-residents and expatriates with limitations or extra documentation.

A person's eligibility for life insurance may also be contingent upon other factors, including:

Smokers

Disabled Individual

People experiencing present-day health problems

Tobacco usage is associated with an increased risk of health problems. To compensate for the higher mortality rate, insurance premiums for smokers are often higher than those for nonsmokers.

An individual's eligibility to acquire life insurance cover is conditional on the nature and severity of their handicap. Factors like mobility, cognitive function, and overall well-being are also considered. Some limitations might impact your rates and coverage options.

Life insurance plans are often accessible to those with pre-existing medical conditions, but pricing and eligibility could vary according to the condition, degree, and overall health. Insurers may require applicants to undergo medical tests to determine their eligibility for insurance and the associated costs.

Types of Life Insurance Plan

The insurance market offers a range of insurance policies that are designed based on specific needs and set goals. To choose best life insurance policy that best fits them, customers need to know the various kinds of life insurance plans

Type of Life Insurance Plan |

Details |

Coverage |

Term Insurance Plans |

Term insurance plans provide pure protection coverage for a specified term, offering a high sum assured at affordable premiums. |

Pure life insurance cover |

Savings Plans |

Savings plans combine insurance coverage with a savings component, allowing policyholders to build a corpus over time while ensuring financial protection for their loved ones. |

Life Insurance cover and savings |

Unit-linked insurance plans (ULIPs) offer a dual benefit: life insurance coverage and investment opportunities. |

Life Insurance cover + Market-linked Investment |

|

Retirement Plans |

Retirement plans, or pension plans, are designed to help individuals build a corpus for their post-retirement years. |

Life Insurance cover + Savings |

Child Insurance Plans |

Child insurance plans are tailored to secure a child's future by providing funds for their education, marriage, or other milestones. |

Life Insurance cover + investment plan |

Employers or associations offer group insurance plans to provide insurance coverage to a group of individuals. |

Life Insurance cover |

|

Whole life insurance is a type of life insurance plan that provides you with financial protection till the age of 99 years. |

Life Insurance cover |

|

Money Back Policy |

Money Back Policy is a type of life insurance that offers the benefit of financial cover as well as investments. |

Life Insurance cover + investment plan |

1. Term Insurance Policy

Your beneficiaries get the sum assured in case of your death during the policy term. However, there is no payout if you outlive the policy term. It features very low premiums. For example - For just a Rs.1000 monthly premium, you can expect to get a life insurance cover of close to a crore.

2. Savings Plans

Savings Plans are a great option to combine insurance coverage with a savings component. These allow policyholders to create a funds corpus over time. It also helps ensure financial protection for loved ones. This way savings plans offer both security and wealth creation.

3. ULIP Plans

A part of the premium you pay goes towards life insurance, and the remainder is invested in various funds such as equity, debt, or a mix of both. The policyholder can decide this as per their risk appetite and preference. ULIPs provide flexibility to switch between funds. As a result, policyholders can easily adapt their investment strategy to changing market conditions. Also, with ULIPs, there is a possibility of higher returns compared to traditional life insurance. They are a great mix of flexibility and potential returns.

4. Retirement Plans

Retirement Plans, also known as pension plans, help individuals build a corpus for post-retirement years. They combine insurance coverage with savings. Thus, offering a steady income stream during retirement. With retirement plans policyholders get financial independence and security in old age.

5. Child Insurance Plans

Child Insurance Plans are wonderful instruments to secure your child's future. They help create a significant corpus for education, marriage, or other milestones. These plans are a combination of insurance coverage with investment options. They ensure financial support to meet future needs and aspirations of children.

6. Group Insurance Plans

The Group Insurance Plans are offered by employers or associations. These provide insurance coverage to a group of individuals, primarily employees or members of an organisation. Group Insurance Plansoffer cost-effective coverage featuring simplified underwriting and administrative ease.

7. Whole Life Insurance Plans

A whole life insurance plan is a plan that provides life cover for the whole life of the policyholder. It may extend to 99 or 100 years of age. It promises to pay a death benefit to the beneficiaries of the policyholder upon his demise and takes care of the financial well-being of the dependents.

8. Money Back Life Insurance Plans

Money Back Policy offers dual benefits to the policyholder. It offers dual benefit of life insurance cover as well as investments. This life insurance plan helps generate income at regular intervals throughout the policy tenure. With it, a policyholder provides financial security to his or her family in the event of death while not making any losses when no claims are made.

Life Insurance Plans are simple to understand!

Tune in to this video to know about our Life Insurance Plans.

Differences Between Types of Life Insurance

Below are some types of life insurance plans:

Term life insurance policy |

Endowment life insurance policy |

Non-linked participating endowment plan |

Unit linked insurance plans (ULIP) |

Non-participating Non-linked endowment plan |

|

Overview |

For the purpose of safeguarding your family's financial interests while you are away |

For the purpose of providing for one's family and accumulating low-risk savings |

For the purpose of providing for one's family and accumulating low-risk savings |

Used to provide for your family's financial needs and grow your wealth according to your risk tolerance |

For the purpose of providing for one's family and oneself financially. There are no changes to the death and maturity benefits. |

Maturity benefits |

No maturity benefits |

Offers maturity benefits |

Offers maturity benefits |

Offers maturity benefits |

Offers maturity benefits |

Death benefits |

Offers death benefits |

Offers death benefits |

Offers death benefits |

Offers death benefits |

Offers death benefits |

Purpose |

Provides pure risk cover |

Provides insurance cover plus low risk savings |

Provides insurance cover plus low risk savings |

Provides insurance cover plus investments |

Provides a fixed insurance cover |

How Does A Term Insurance Policy Work?

A term insurance policy lends coverage for a specific period, which could vary from person to person. If the policyholder passes away within this term, the beneficiaries receive the death benefit. For example, Raj, a 30-year-old, buys a 20-year term policy with a ₹1 crore death benefit. He pays an annual premium of ₹10,000 to keep the policy active. If Raj passes away at 40, his beneficiaries receive the said ₹1 Crore. The same amount will be paid if Raj expires at 35 or 45 years. The death benefit amount remains the same, irrespective of the total premium paid by the policyholder. However, this applies only if the policyholder has died within the covered term. Now, if Raj survives the 20-year term, the coverage ends, and no payout is made unless he has opted for a return of premium rider.

Life Insurance Coverage Amount Explained

The suitable amount of coverage for a life insurance policy is crucial to guarantee that loved ones' finances are safeguarded in the event of the policyholder's demise. There are a lot of things to think about when determining the amount of coverage in life insurance cover:

Current and Future Income

To make sure that the policyholder's loved ones can keep up with their current lifestyle and take care of ongoing financial obligations like rent or a mortgage, as well as cover basic living expenses, you need best life insurance policy with a payout that can cover both your current and future income.

...Read More

Loans and Debts

The sum insured must account for all of the policyholder's present obligations and liabilities. Mortgages, automobile loans, student loans, and credit card debt all fall under this category. Loving ones left behind may rest easy knowing that these debts will be paid off with the death benefit.

...Read More

Financial Goals

It is important to take into account the policyholder's financial goals, such as covering education costs, caring for aging parents, or saving for retirement. Together, these goals and the coverage amount have the potential to provide financial stability for the family so that they may realize their aspirations.

...Read More

End-of-Life Expenses

Be sure to include in the coverage amount any last expenses, such as the cost of the funeral and burial, any medical bills, and any costs related to the estate settlement. If the death benefit covers these expenses, it can help the family financially immediately.

...Read More

Other Coverage

If you already have a policy, such as group life insurance or an employer-sponsored plan, you should modify your coverage level accordingly. The goal is to make sure the family is financially protected without going overboard with insurance or having redundant policies.

...Read More

Benefits of Life Insurance Plans

Here are some of the most common benefits of investing in Life insurance plans:

Financial Support

An important safety net, life insurance provides financial support to policy beneficiaries in the event of the policyholder's death. Funeral costs, bills, mortgage payments, and ongoing living expenses may all be helped out by the death benefit, relieving loved ones of some financial burden during this difficult time.

...Read More

Loan Collateral and EMI Payments

Policyholders may be able to receive loans at more favorable interest rates if they use best life insurance policy as collateral. In addition, the death benefit may be used to settle the insured's outstanding bills and EMI payments, which helps alleviate financial strain on families left behind.

...Read More

Tax Benefits

In life insurance plans, the premiums paid are tax deductible under Section 80C of the Income Tax Act. In addition, the death benefit is not taxable according to Section 10, thus beneficiaries may have even more financial peace of mind and savings (10D).

...Read More

Additional Benefits

In addition to financial security and tax advantages, life insurance plans other benefits such as:

Easy customization of insurance coverage to specific needs with the use of riders.

Possibility of accumulating a wealth corpus over the years with some of the best life insurance policy plans such as whole life policies. These funds are available to policyholders via policy withdrawals or loans, providing them with liquidity and financial flexibility.

Depending on the policyholder's financial situation and personal preference, several life insurance plans provide premium payment options such as monthly, quarterly, or yearly.

...Read More

Important Terms About Life Insurance Plans in India

Here are some basic terms frequently used in the context of Life insurance plans:

Sum Assured

It is the basic coverage amount agreed upon between the two parties when the policy is purchased. The policyholder chooses this sum based on their needs and financial goals. It helps provide financial security to the beneficiaries of the insured and can be used to meet expenses and debts, ensuring their standard of living is maintained after the policyholder's demise.

...Read More

Life Assured

The individual whose life is insured under the policy is called life assured. The death of the life assured leads to the payment of death benefits to the beneficiaries.

...Read More

Death Benefit

Those who are insured will receive a lump sum benefit from the insurance company if the insured dies before the policy has expired. This sum is called the death benefit.

...Read More

Maturity Benefit

After the life insurance policy expires, the policyholder is entitled to the maturity benefit. All profits and bonuses earned during the policy period are summed up to form the expected guaranteed payout.

...Read More

Riders

Policyholders may augment their policy by choosing additional benefits known as riders. Standard riders include critical illness coverage, accidental death coverage, disability coverage, premium waiver, and others.

...Read More

Free Look Period

The free look period gives policyholders 30 days after the policy's issuing date to examine its terms and conditions. If dissatisfied, an insurer can cancel the policy and get a refund after deducting certain expenses.

...Read More

Lapsed Policy

Insurance is considered expired or lapsed if the policyholder does not pay by the due date set in the policy. Before renewing their policies, policyholders might be required to clear any unpaid premiums or meet certain requirements.

...Read More

Grace Period

Policyholders are given an extension of time beyond the premium payment deadline so that they can continue to receive cover. This extra time is called the grace period. As a rule, it is a 15-30 days period that prevents the insurance from lapsing.

...Read More

Revival Period

The duration in which a lapsed policy can be reinstated is called the revival period. This can be done by paying overdue premiums and fulfilling any other requirements the insurer sets.

...Read More

Claim Process

A certain procedure needs to be followed for the beneficiaries to access the death benefit. This is called the claim process after the life insured passes.

...Read More

Exclusions

Some conditions, called exclusions, will prevent the life insurance policy claim from being paid. Exemptions that might vary from policy to policy include suicide within the initial term of the insurance cover, engaging in risky activities, and pre-existing medical conditions.

...Read More

Policy

A policy is a legally binding contract between an insurer and the insured. It specifies the obligations and rights of each party. This agreement stipulates the duties and the rights of the insurer and the policyholder.

...Read More

Policy Tenure

The period of validity or tenure of a life insurance policy, also known as its term, is the period during which the policy is effective. The specifics depend on the policy type and the needs of the policyholders.

...Read More

How To Choose A Life Insurance Policy?

Check out these simple steps to help you make an informed decision:

Assess Your Financial Needs

First, take a good look at your financial situation. Think about your family's daily living expenses, any outstanding debts, future education costs for your kids, and other financial commitments. This will help you figure out the right amount of coverage, or sum assured, to keep your loved ones secure.

...Read More

Check and Compare Different Types of Life Insurance Policies

There are many life insurance policy India plans to choose from, each with its own benefits. A term life insurance policy is affordable and provides coverage for a set period. The whole life and universal life insurance plans offer lifelong coverage. They also have an added savings component. Unit-linked insurance plans (ULIPs) on the other hand combine insurance with investment opportunities. Compare these options to find the one that fits your needs and budget the best.

...Read More

Check the Provider's Reputation

If you are looking for the best life insurance policy in India, it is important that you go with an insurance provider who enjoys a good reputation for reliability and financial stability. Look into the company's Claim Settlement Ratio (CSR), which shows the percentage of claims paid out versus the total claims received. A higher ratio is a good sign that the insurer is dependable.

...Read More

Read Reviews

Finally, check out reviews and testimonials from current policyholders. Their experiences can give you insight into the company's customer service, ease of claim processing, and overall satisfaction. Online forums, review sites, and financial advisory platforms are great places to start.

...Read More

Factors to Evaluate Before Deciding on Life Insurance Protection

Before you decide which life insurance plan you want to go with, here are some important factors to consider:

Goals

Identify your long-term financial goals, such as providing for your family, funding your children's education, or securing a comfortable retirement. Understanding your goals helps determine the coverage amount needed.

Age

Your age significantly impacts the type and cost of life insurance. Younger individuals typically pay lower premiums and can benefit from longer-term policies, while older individuals may need to consider policies that offer lifelong coverage.

Debts

Evaluate your outstanding debts, such as mortgages, personal loans, or credit card balances. Ensure your life insurance coverage sufficiently cover these liabilities, preventing financial burden on your family.

Stable Income

Consider your income stability and future earning potential. A steady income allows you to maintain regular premium payments, while fluctuating income might require flexible policy options to avoid lapses in coverage.

Remaining Employment Tenure

Assess your remaining years of employment and potential retirement age. Life insurance can bridge the financial gap between your working years and retirement, providing peace of mind that your loved ones are protected regardless of your employment status.

Dos And Don'ts When Dealing With Life Insurance Policies

Here are some important do’s and don’ts to keep in mind when dealing with life insurance policies. These guidelines will help you make the best choices for your financial security:

Do’s |

Don’ts |

Check the insurer's reputation: Research the insurance company's claim settlement ratio and financial stability. |

Don't ignore reviews and testimonials: Pay attention to customer feedback to avoid unreliable insurers. |

Read all policy documents very carefully: Understand the terms, conditions, and exclusions of your policy. |

Don't overlook the fine print: Make sure you're aware of all policy details to avoid surprises later. |

Make timely premium payments: Stay on top of your premium payments to keep your policy active. |

Don't miss premium payments: Missing payments can result in policy lapses and loss of coverage. |

Keep your beneficiaries informed: Ensure your beneficiaries know about the policy and how to claim it. |

Don't forget to update your policy: Update your policy regularly to reflect changes in your life circumstances. |

Seek professional advice wherever required: Consult with a financial advisor to make informed decisions. |

Don't hesitate to ask questions: Clarify any doubts with your insurer or advisor to ensure you understand your policy fully. |

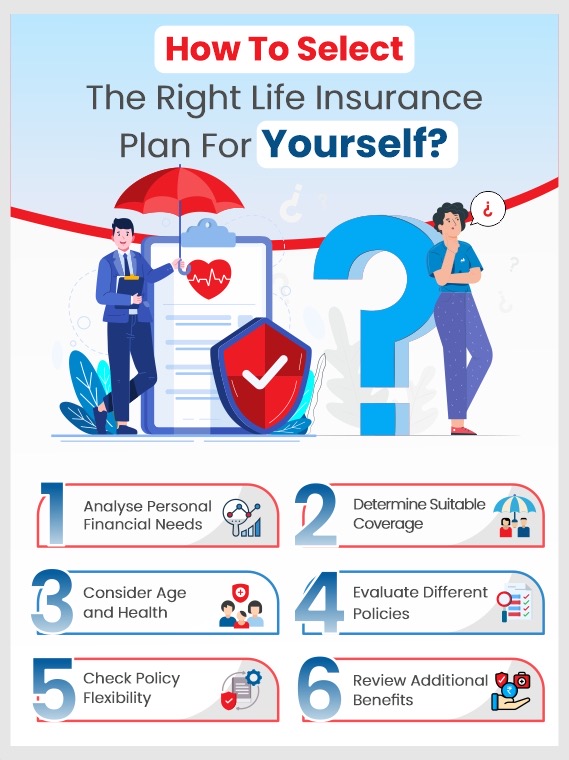

How to Select the Right Life Insurance Plan for Yourself and Your Family?

Selecting life insurance policy plans becomes a crucial thing if you really care about leaving your loved ones secure for the future. Here are some factors to consider:

How To Select The Right Life Insurance Plan For Yourself:

- Analyse Personal Financial Needs: Consider your living expenses, debts, and financial commitments.

- Determine Suitable Coverage: Choose a coverage amount that reflects your current and future financial needs.

- Consider Age and Health: Younger and healthier individuals can often get lower premiums.

- Evaluate Different Policies: Compare term, whole, and universal life insurance options to match your financial goals.

- Check Policy Flexibility: Look for policies that allow for adjustments in coverage or premium payments.

- Review Additional Benefits: Consider riders for added protection like critical illness or disability.

How To Select The Right Life Insurance Plan For Your Family:

- Assess Family Financial Needs: Calculate your family’s living expenses, future education costs, and other financial obligations.

- Determine Coverage Amount: Ensure the sum assured is enough to cover all their needs and debts.

- Consider Future Goals: Think about long-term goals of your whole family including your children's education, marriages, home ownership, and retirement.

- Evaluate Policy Types: Do a thorough comparison of term life, whole life, and ULIPs to find the best fit for your family's needs.

- Review Policy Features: Look for additional benefits like riders for critical illness or accidental death.

Evaluate different policies, whether you are buying life insurance for yourself or your family. Consult a financial advisor for customised advice based on your personal financial situation. With due diligence, you will be able to select the best life insurance policy in India.

How much Life Insurance cover does one need?

Here are some factors to consider that will help you determine adequate coverage from your best life insurance policy in India:

Number of working years

A life insurance policy acts as an income replacement plan if the insurer passes away. Therefore, it is important to consider the number of working years you are left with and should consider catering to. The insurance coverage amount should be enough to provide your family with financial support for those many years.

Regular Expenses

Calculate your family’s monthly budget and spends including housing (mortgage or rent), utilities, food like groceries, education, healthcare, and so on. The insurance amount should be enough to pay for these expenses during the period.

Landmark Stages in Your Family’s Life

Think about the landmark’s your family will have in future like weddings, retirements, and college graduations. If you want to achieve your family's financial goals even after your death, make sure to adjust the amount of coverage of life insurance policy India to fit the future demand.

Life Insurance Plans offered by HDFC Life

Here are few life insurance plans offered by HDFC Life:

Life Insurance Plan |

Description |

HDFC Life Click 2 Protect Super |

A comprehensive term insurance plan offering financial protection to your loved ones at affordable premiums. |

HDFC Life Sanchay Plus |

A savings cum insurance plan that provides guaranteed returns and financial security for your family's future. |

HDFC Life Click 2 Wealth |

A unit-linked insurance plan (ULIP) that offers the dual benefits of life insurance coverage and investment opportunities to help you achieve your long-term financial goals. |

HDFC Life Guaranteed Pension Plan |

A retirement plan designed to provide a regular income stream and financial stability during your golden years. |

HDFC Life YoungStar Udaan |

A child insurance plan that secures your child's future by providing funds for education, marriage, or other milestones, even in your absence. |

What Is Human Life Value, And Why Should You Consider It Before Deciding On Your Life Cover?

Human Life Value (HLV) is a financial concept used to evaluate the economic worth of a person, keeping in view their future earnings, expenses, liabilities, and savings. It is usually used to assess the value of the financial contribution a person makes to their family. It becomes a vital factor in determining the right amount of life insurance coverage one may need.

Why Consider HLV Before Deciding on Your Life Cover?

Here are some ways HLV helps decide your life cover:

- Calculating Accurate Coverage: With HLV, you can expect an accurate estimate of the life insurance coverage you need to secure your family financially in your absence.

- Assessing Future Financial Needs: HLV considers your future income potential and financial responsibilities. This helps ensure that your family’s future needs are adequately covered.

- Helping with Repayment of Debt: HLV takes into account your outstanding debts, ensuring that your life cover is sufficient to settle these liabilities without burdening your family.

- Peace of Mind: With HLV, you know that your life insurance coverage is based on a comprehensive analysis of your financial worth. This offers peace of mind that your family will be taken care of in your absence.

To calculate your Human Life Value, you can use an HLV calculator. Mention your income, expenses, liabilities, and savings into the tool to determine the appropriate life cover amount for your financial situation.

Should One Buy More Than One Life Insurance Policy?

This decision completely depends upon your present financial health and future needs and goals. Whether you should have multiple policies depends on how much coverage you are seeking. More policies, on the one hand, can widen the coverage, but on the other, they can be a financial burden in your present circumstances.

Having multiple policies works for those seeking to reduce risk and ensure that they have another policy to bank upon in case of delayed or rejected claim settlement from one.

Still, managing multiple policies can be challenging, with risks of delayed or missed premium payments, leading to coverage lapses. Hence, it is best to assess the risks and rewards of this decision before going ahead with multiple policies.

Riders in Life Insurance

Policyholders have the option to add extra provisions to the basic life insurance policy coverage they have, by purchasing life insurance riders. Life insurance policy riders help policyholders tailor their coverage to their specific needs and financial goals.

Riders bolster financial security for the policyholders and their beneficiaries by including one or all of the following -

Accidental Death Benefit Rider (ADB)

Waiver of Premium Rider

Critical Illness Rider

Term Conversion Rider

Child Term Rider

Accelerated Death Benefit Rider

Long-Term Care Rider

Your insurance provider may name these differently. It is therefore best to check with your insurer for the available riders.

Steps to Buy Life Insurance Policy Online

Here are the steps to buy the best life insurance policy online:

Find the insurance plans that best suits your needs by comparing costs, terms, coverage, premiums, other benefits and features of life insurance plans, offered in India

...Read More

Use an online calculator to estimate your premium.

...Read More

Before you submit your application online, double-check that you've entered all of your personal and contact details correctly. These include - name, age, gender, occupation, and any relevant medical history.

...Read More

It is necessary to provide scanned copies of documents, including domicile document, age, income, and identity proofs.

...Read More

If your insurance provider and preferred plan require it, you may be requested to undergo a medical examination.

...Read More

Prior to making a payment, make sure you have read the whole policy, including all of the small print.

...Read More

Pay the premium using a safe online payment method, such as a credit/debit card, digital wallet, or net banking.

...Read More

Once the payment is processed and the application is approved, you will receive the best life insurance policy documents via courier or email.

...Read More

Be sure to read the papers thoroughly before putting it away for future reference.

...Read More

Documents Required to Buy a Life Insurance Plan in India

-

PAN card

-

Residence Verification

-

Birth Certificate

-

Income Tax Returns

-

Medical Records from the Past

How to Save Tax with Life Insurance Policy?

In addition to providing financial security, a life insurance cover also offers tax benefits. Read on to find out how:

Deductions under Section 80C:

Deductions under 80C of the Income Tax Act Premiums paid towards life insurance policies are eligible for tax deductions. There is a maximum deduction of INR 1.5 lakh per financial year.

Maturity Proceeds:

The maturity proceeds from life insurance policies are tax exempted under Section 10(10D) of the Income Tax Act. However, the premium must not exceed 10% of the sum assured in any year during the policy term.

Rider Premiums:

Premiums paid towards riders are also eligible for section 80d.

Tax-Free Death Benefit:

According to the Section 10(10D) of the Income Tax Act, the death benefit received by the nominee/legal heir is tax-free under.

Tax-Free Surrender Value:

When a policyholder surrenders the policy before its maturity date, the surrender value/amount received is tax-free under Section 10(10D) (although conditions apply here).

Pension Plans:

Premiums paid towards life insurance pension plans are eligible for tax deductions under Section 80CCC. However, there is an overall limit of INR 1.5 lakh on these under Section 80C.

Exemption for HUF:

Life insurance premiums paid for members of an HUF are also tax benefited under Section 80C, subject to the overall limit.

How to File a Life Insurance Claim?

When filing a claim for a life insurance policy you can file via the following modes:

Online claim:

To submit your claim online, visit the HDFC Life Claims section on the website. Verify the policy details, submit details of life assured and the nominees to start the claims process.

Claim At Branch:

To submit a claim at your nearest branch download the appropriate claim form from the website and fill correctly. Submit along with supporting documents at the nearest HDFC Life branch for seamless claim filing.

Claim Via Phone:

To initiate claim settlement process via phone, you can call the Claim helpline.

In case of natural death following needs to be provided:

Mandatory documents

Original policy document (Not necessary in case of dematerialised policy document)

Death Claim Form

Death certificate issued by local authority

Claimant's passport size photograph

Personalized Cancelled Cheque or Bank Passbook (with Printed A/c no, IFSC & Name account holder)

Claimant's Valid Identity Proof

Claimant's Valid Address Proof

Claimant's PAN CARD/Form 60 (if PAN Card not available)

Employer’s certificate (Form) for Life Assured, if employed (not required for pension/ annuity plans)

Additional Documents

Medical cause of death certificate

Medical records for all the treatments taken in the past. (Admission notes, History / Progress sheet, Discharge /Death summary, Test reports, etc.)

Note:

Self-Attestation is required on any photocopies of the KYC or any other document copies submitted by the Claimant.

HDFC Life may call for documents apart from the above (case specific).

In case of maturity claim you need to provide:

A cancelled cheque

Life insurance policy certificate

KYC proofs like Aadhar card, PAN card, or any other required document

How to Avoid Life Insurance Claim Rejection?

Here is what you must know in order to get your life insurance policy claim approved for most life insurance plans India:

Be honest when filling out a life insurance policy India application; this is especially crucial when answering questions about your health, lifestyle choices, and other private matters.

Your insurance will remain active and your claims will not be refused if you pay your premiums on time.

Make sure you read and completely comprehend the policy's terms, restrictions, and exclusions to avoid having your claim refused because of a misunderstanding.

Make sure the person designated as your representative has the most recent contact information and is familiar with the claims process in the event of your death.

Any change in health status or significant lifestyle decisions should be disclosed in order to prevent claim rejection due to non-disclosure.

Why Should Women Consider Investing In A Life Insurance Policy?

Women should consider investing in a life insurance policy to ensure financial security for their families and themselves. As primary or secondary income earners, women contribute to household finances.

Life insurance provides a safety net. It covers expenses, debts, and future financial needs like kids’ education and retirement. It also offers peace of mind, knowing loved ones will be protected in case of one’s untimely death.

For stay-at-home mothers, life insurance can help cover the cost of services they provide. These may include childcare and household management.

Crucial Situations When You Should Consider Reviewing Your Policy

Here are some situations when you need to consider reviewing your life insurance policy:

Situation |

Reason To Review Your Policy |

Getting married |

Marriage introduces new financial responsibilities and dependents. Therefore, it is a must to reassess coverage to ensure adequacy. |

Having children |

With parenthood your financial obligations increase. This makes it important to ensure adequate coverage for your kids’ future. |

Taking a loan |

When you take a large loan, it is wise to take additional coverage to protect against financial burdens. |

Dependents facing medical conditions |

Medical issues among dependents can increase financial strain. It requires enhanced coverage for financial security. |

FAQs on Life Insurance Policy

1 What is life insurance policy?

A life insurance policy is a contract/agreement between the policyholder and the insurance company. Under this policy, the insured commits to paying premiums for a pre-determined period to the insurer. In exchange, the insurer guarantees to pay a certain sum as a death benefit to the insured’s beneficiaries.

2 What are the 3 main types of life insurance?

There are generally three types of life insurance:

Term Insurance

Whole Life Insurance

Universal Life Insurance

3 Why is life insurance plan useful?

Life insurance is useful as it offers financial protection to your loved ones in the event of your death. It ensures that your dependents are financially secure. The benefits help them maintain their standard of living even after you are not there. Additionally, life insurance can help cover expenses such as funeral costs, outstanding debts, loan payments. It also helps with future financial needs like education or retirement funding.

4 How much does life insurance policy cost?

The cost of life insurance varies based on several factors. These include - age, health, lifestyle, coverage amount, type of policy, and term length. Generally, younger and healthier individuals pay lower premiums compared to older or less healthy individuals.

5 What are the different options available for premium payments?

Insurance companies offer various options for premium payments. Some of the most common ones include - annual, semi-annual, quarterly, and monthly payments.

6 What are the consequences of non-payment of premium?

Non-payment of premiums has serious consequences on your life insurance policy. If you miss premium payments, your policy may lapse. As a result you lose coverage and any accumulated cash value. Some policies offer a grace period during which you can make late payments to avoid lapsing. However, if you fail to pay within the grace period, your policy may terminate.

7 How can I file the claim in case of insured person's demise?

A death claim can be filed online or at the nearest branch. In case of natural death following needs to be provided:

Mandatory documents

Original policy document (Not necessary in case of dematerialised policy document)

Death Claim Form

Death certificate issued by local authority

Claimant's passport size photograph

Personalized Cancelled Cheque or Bank Passbook (with Printed A/c no, IFSC & Name account holder)

Claimant's Valid Identity Proof

Claimant's Valid Address Proof

Claimant's PAN CARD/Form 60 (if PAN Card not available)

Employer’s certificate (Form) for Life Assured, if employed (not required for pension/ annuity plans)

Additional Documents

Medical cause of death certificate

Medical records for all the treatments taken in the past. (Admission notes, History / Progress sheet, Discharge /Death summary, Test reports, etc.)

Note:

Self-Attestation is required on any photocopies of the KYC or any other document copies submitted by the Claimant.

HDFC Life may call for documents apart from the above (case specific).

8 What is a 5 year life insurance policy?

A 5-year life insurance policy is a short term insurance that keeps the insurer covered for five years. It offers tax benefits and death benefits, but there is no cash out in this case. If the policyholder passes away while the policy is valid, the death benefit amount is paid out to the beneficiaries.

9 When can I start to pay the life insurance premiums?

You must pay your first premium to activate your life insurance policy. The premium payment activates your cover. You may pay your premium monthly, quarterly, semiannually, or annually, depending on the policy's terms and your choice.

10 Will I have to pay tax on my life insurance policy's maturity benefit?

According to Section 10(10D) of the Income Tax Act, 1961*, the maturity benefit from a life insurance policy is non-taxable if the premium you paid is either not more than 5 lakh a year or does not exceed 10% of the sum assured.

11 What do you mean by paid-up value in life insurance?

The value of the sum assured after premium payment has been stopped by the policyholder (before the maturity date) is called the paid-up value. In such a case, the policy will remain in force with a reduced death benefit. This benefit amount is then based on the premiums paid and the length of time the policy has been active.

12 Which type of life insurance plan is the most affordable?

A term life insurance plan is the most affordable type of life insurance plan. It offers coverage for a specific period, say, 10 years or 20, or 30 years. There is a death benefit if the policyholder dies within the term. Premiums for term insurance are lower compared to whole life insurance.

13 How long does life insurance take to payout?

Life insurance payouts typically take between 15 to 60 days after a claim is filed. The variation in timelines comes from various factors including the insurance company's processes and the completeness of the submitted documentation. Delays can also take place if there is any investigation required or if the necessary paperwork is incomplete.

14 What happens if I outlive my life insurance policy term?

If you outlive the term of your life insurance policy, the outcome depends on the type of policy you have. If it is a Term Life Insurance, the cover ends without any payout unless the policy has a return of premium feature. In the case of Whole Life Insurance and universal life insurance, as long as you pay the premiums, the policy cover is maintained, and the accumulated cash value provides a health benefit whenever the insurer passes away. If yours is an endowment policy, you receive a sum assured plus bonuses, if any, when the policy matures.

Here's all you should know about life insurance.

We help you to make informed insurance decisions for a lifetime.

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance solutions - protection, pension, savings, investment, annuity and health.

Popular Searches

- term insurance plan

- term insurance calculator

- Investment Plans

- savings plan

- ulip plan

- retirement plans

- health plans

- child insurance plans

- group insurance plans

- saral jeevan bima yojana

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- benefits of term insurance calculator

- what is term insurance

- why to invest in life insurance

- Ulip vs SIP

- tax planning for salaried employees

- how to choose best child insurance plan

- tips for buying retirement plan

- 1 crore term insurance

- HRA Calculator

- Annuity From NPS

- 2 crore term insurance

- 5 crore term insurance

- 1.5 crore term insurance

- Retirement Calculator

- Pension Calculator

- What is Investment

- Best Investment Plans

- benefits of term insurance

- types of life insurance

- types of term insurance

- Endowment Policy

- Benefits of Life Insurance

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- life insurance

- life insurance policy

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- Saving Schemes

- Ulip for NRI

- Life Insurance for NRI

- Investment Plans for NRI

- what is nominee in insurance

- features of life insurance

- Best Term Insurance Plan for 1 Crore

- features of term insurance

- personal accident insurance

^ Available under Life & Life Plus plan options

##Individual death claim settlement ratio by number of policies as per audited annual statistics for FY 2023-24.

#Provided we have received all the relevant and required documents and no further investigation is required. Claim settlement process would be completed within stipulated timelines once the claim request is approved

***Online Premium for Life Option for HDFC Life Click 2 Protect Super (UIN: 101N145V04), Male Life Assured, Non-Smoker, 20 years of age, Policy term of 25 years, Regular pay, Annual frequency, exclusive of taxes and levies as applicable. (Monthly Premium of 622/30=20.7).

**7% online discount available on 1st year premium only

@As per integrated annual report FY23-24, available on www.hdfclife.com. As of May 2024

ARN - DM/07/24/13530